The lowest listings in 30 years, a booming population and soaring rents are driving the Perth property market and luring investors from around Australia and internationally.

A range of dubious records are driving Perth’s property values to record highs.

Listings are at the lowest level in 30 years, with fewer than 5,000 properties on the market. The number of REIWA listings has declined to 4,931, a massive drop of 40 per cent on a year ago.

In September, Perth’s median house value reached $646,700 – a 9.0 per cent increase on the same time last year, according to CoreLogic.

The record low vacancy rate is also attracting investors seeking high rents and first home buyers trying to escape them.

Perth’s vacancy rate dropped to 0.4 per cent in September, according to SQM Research data released Tuesday (17 October), a decline of 0.1 percentage points from the same time last year. This is the lowest vacancy rate among state capitals, well below the national level of 1.1 per cent and a balanced market’s 2-3 per cent range.

“Long term trends show rental listings tend to decline in the lead up to the end of the year, so the vacancy rate is likely to remain low in the coming months,” REIWA CEO Cath Hart said.

Tight conditions in Perth’s rental market were being driven by low supply and high demand.

Suburbs with the most growth in the last three months – Houses.

Source: REIWA. Houses, > 1 HA, 20 or more settled sales June-August 2023 as at 13 October 2023

Julie Kelley, Global Sales and Marketing Manager for aussieproperty.com, said rapid population growth and investor interest from overseas and the eastern states was behind Perth’s strong property market performance.

“With more people arriving in Perth every day, it is bolstering demand for rental properties while the ongoing delays within the building industry are keeping people in their rental properties longer, impacting the usual market turnover,” she said.

“While we continue to see heightened interest from eastern states investors and the decline in the number of rental properties in the market stabilises, demand continues to exceed supply.

“It’s a problem that’s been years in the making and won’t be solved overnight.”

Perth’s property price growth for the September quarter of 3.6 per cent was behind only Adelaide (4.3 per cent) and Brisbane (3.9 per cent).

CoreLogic’s research director, Tim Lawless, attributed Perth and the smaller capital cities’ growth rates outpacing Sydney and Melbourne to the premium housing sector losing some steam after leading the recovery cycle.

Investors pouring into Perth

WA is experiencing the fastest population growth rate of any Australian state and territory, growing by 2.8 per cent to 2.855 million in the year to March 2023. The March quarter saw one of the biggest recorded population increases at 0.9 per cent.

The scant number of properties that are finding their way onto the market are being snapped up in record time too. The average days-on-market is 13 days, with suburbs such as Leeming, Harrisdale and Gwelup at eight days, Palmyra and Bicton at seven days, and Shenton Park at a blink-and-you’ll-miss-it four days, according to REIWA.

Ms Kelley said that with such limited housing stock, competition has increased among all buyer segments, including first home buyers, investors, owner occupiers, downsizers and migrants.

“We are seeing an influx of overseas and interstate migration; they are cashed up and needing somewhere to live.

“Investors are across all types of property too; from land banking for future development to property that is primed for fast capital growth, as well as affordable housing with attractive rental yields.”

Property investors have played a big role in driving Perth property prices higher.

The latest Australian Bureau of Statistics lending figures for August 2023 show the total value of property investment loans in Western Australia totalled $827 million, the highest monthly figure for property investment since early 2015.

Catherine Doherty, WA Branch Manager, Property Club, said if current trends continue the overall property investment in the state could soon top $1 billion per month.

“In particular the lower to mid-priced sections of the Perth real estate market should perform very well over the coming year as they are viewed as extremely affordable by eastern states investors.

“At a micro level, Property Club also predicts that affordable suburbs that will be the focus of new infrastructure, such as new rail links, will attract significant investor activity and as a result rising property values over the coming years.”

“Despite this large jump in property investment activity we predict the rental market in Perth will continue to remain very tight because of the huge influx of people into the state from interstate and overseas,” Ms Doherty said.

“We predict vacancy rates will continue to remain low in Perth, resulting in rising rents during 2024 as well as increases in property prices.”

With renters trying to get a foot on the property ladder at a time of rising house prices, units were becoming a target of many buyers.

CoreLogic data showed Perth’s median unit price was $437,800 in September, a 6.5 per cent increase from September 2022.

Suburbs with the most growth in the last three months – Units.

“While Perth is still one of Australia’s most affordable capital cities, some homebuyers are starting to find it more challenging to enter the detached housing market,” he said.

“This is where unit and strata properties come into play, as they typically offer a more affordable entry point.”

Beyond affordability, Mr Gavalas said unit and strata properties also offered an increasingly attractive proposition for many buyers, as they typically require less maintenance than houses.

“The reduced maintenance responsibilities can be particularly appealing to investors, as it can translate to lower ongoing costs and potentially higher rental yields,” he said.

Perth means business

As well as permanent residents migrating to the state, there has also been a marked increase in business travellers to the state, which in turn attracts further property investment.

Perth has seen the largest growth in incoming international business travellers over the past year, with a 34 per cent increase between June-December 2022 and January-July 2023.

Perth is in the running to outpace Melbourne in international business travellers this financial year, as Victoria’s capital city only increased its arrival figures by seven per cent for the same period. Likewise, Sydney’s growth in total international business travellers only increased by eight per cent.

“Corporate Traveller data from earlier this year revealed that the construction industry is the leading sector for travel spend, having increased its expenditure by 98 per cent between the first quarter of 2022 and 2023.

“It’s a clear indicator that business is booming with more travel required for employees and stakeholders needing to visit new sites and projects across Australia.

“With Western Australia’s continuing prosperity in mining and resources, it’s no surprise business travellers from interstate and international locations are flocking to the state for this reason.” Mr Walley said.

Article Q&A

Why are Perth property prices rising?

Listings in Perth are at the lowest level in 30 years, with fewer than 5,000 properties on the market. The near-record low vacancy rate is also attracting investors seeking high rents and first home buyers trying to escape them.

What is the vacancy rate in Perth?

Perth’s vacancy rate dropped to 0.7 per cent in September, a decline of 0.1 percentage points from August.

Where are house prices rising fastest in Perth?

Over the last three months, the fastest rising house prices were in Cottesloe (9.6 per cent), followed by Pearsall, Hammond Park, Ferndale and Wannanup.

Where are unit prices rising fastest in Perth?

Over the last three months, the fastest rising unit prices were in Mosman Park (8.6 per cent), followed by North Fremantle, Palmyra, Glendalough and Burswood.

Applied wisely, debt recycling can reduce tax liability and increase investment opportunities.

In the eyes of the Australian Taxation Office (ATO), not all debt is equal.

In Australia, the ATO permit taxpayers to claim a tax deduction for interest incurred on investment-related loans. Interest, however, on private (as opposed to investment-related) loans is not tax deductible.

So, what exactly are considered tax deductible investment loans?

By and large these are loans taken out for the purpose of acquiring income producing assets or investments. It could be, for example, a mortgage to acquire an investment property, or a margin loan to acquire listed shares.

So, what loans then are considered private in nature and why is there no tax deduction allowed for such loans?

Private loans typically exist when non-income producing assets or investments are bought. Common examples are acquiring your family home, as well as a car or boat, even outstanding credit card debt.

To be considered tax deductible, there generally must exist a nexus between an expense to assessable income. In the case of loan interest, the necessary nexus is the taxable investment income being earnt, for example rental income, dividend income, etc.

There is no taxable income to ascertain from your family home and other such personal chattels. As there is no tax nexus, any interest incurred is thereby non-deductible.

But does the tax deductibility status of a loan really make that much difference? After all, if you pay $10,000 of interest, then whether it is personal or investment related you have still paid $10,000 … correct? Well, not exactly.

It is true that in both circumstances you have paid the bank or finance company $10,000 in interest, but it is the after-tax cost of that interest that is most relevant.

To illustrate:

An individual has $150,000 of taxable income. This places them in the 39 per cent (being 37 per cent + 2 per cent Medicare levy) tax bracket.

A $10,000 tax deduction at 39 per cent equates to a $3,900 tax refund. The after-tax interest cost is therefore $6,100 (being $10,000 – $3,900).

If on the other hand the loan was of a private non-tax-deductible nature, then that same individual must actually earn $16,393 (being $10,000 / (1 – 39 per cent)).

At 39 per cent marginal tax rate, earning $16,393 will result in $6,393 in income tax being paid (being $16,393 x 39 per cent), thus leaving $10,000 remaining with which to pay the bank or the financing company.

In other words, the “same” $10,000 of interest will either cost you $16,393 if the loan were personal in nature otherwise $6,100 if the loan were investment in nature.

Table 1: Comparison of $10,000 interest paid at various marginal income tax rates – $10,000 Interest Paid.

Marginal Tax Rate (Incl Medicare)

0%

21%

34.5%

39%

47%

Private Loan

$10,000

$12,658

$15,267

$16,393

$18,868

Investment Loan

$10,000

$7,900

$6,550

$6,100

$5,300

Table 2: Effective interest rate of a 7% p.a. loan at various marginal income tax rates – 7% Interest Rate.

Marginal Tax Rate (Incl Medicare)

0%

21%

34.5%

39%

47%

Private Loan

7.00%

8.86%

10.69%

11.47%

13.21%

Investment Loan

7.00%

5.53%

4.58%

4.27%

3.71%

For someone earning above the top marginal tax rate of 47 per cent, private debt is almost a staggering four times as expensive as investment debt!

So are there any ways to be able to convert private non-tax-deductible interest into tax-deductible investment interest. The short answer is yes and one such strategy is a concept known as debt recycling.

Debt recycling explained

At its heart, the principal of debt recycling is to physically pay down a private loan and physically redraw it to fund the acquisition of an income producing investment. This can be done in one go or, alternatively, piecemeal via multiple loan splits.

Case study 1:

Several years ago, a person bought their family home. Their remaining mortgage currently stands at $1 million. They have $250,000 in savings currently in their bank account. They are wanting to invest the full $250,000 into dividend-paying listed shares.

The process starts by splitting their home loan into $750,000 and $250,000, paying down the $250,000 loan to a nominal $1 using cash savings, and subsequently redrawing the funds to acquire the listed shares.

There is still $1m in total loans, as the strategy of debt recycling is not necessarily about borrowing more, rather converting the characteristics of the original loan.

So, from the original position of $1 million in private loans there is now $750,000 in private loans and $250,000 in tax deductible investment loans – tax deductible by virtue of having created the necessary nexus to assessable dividend income

Case study 2:

Similar to scenario 1, a person has a $1 million loan remaining on their main residence home. They have accumulated $1 million in savings, which they were planning to put towards buying a $1.5 million investment property.

In this situation further borrowing of $500,000 is required to be able to acquire the investment property (putting aside stamp duty and other transaction costs).

Paying down the existing $1 million private main residence home loan in full (to a nominal $1) then redrawing back out the full $1 million to contribute to the investment property purchase results in 100 per cent of private debt having been eliminated. While the original loan still exists, it has been completely recharacterised into tax deductible investment debt.

A superior tax outcome has therefore been achieved, as the $1.5 million investment property now has $1.5 million tax deductible loans attached to it, as opposed to the initially proposed $500,000 loan.

Although the underlying security or collateral for the original $1 million loan continues to be the main residence, the debt recycling strategy has changed the use of the funds. The interest on monies borrowed is attached to the asset acquired. The process of paying down the original loan effectively extinguishes the original use of the funds to buy the main residence and replaces it with the new use, being to buy the investment property.

There are several variations to the above two case studies that can assist with a debt recycling strategy, including selling existing (typically liquid) investments to generate sufficient cash holdings to pay down private loans.

Tricks and traps of finance repositioning

As with any tax strategy, be sure to obtain professional advice as it is imperative that the arrangement be structured appropriately to not only enhance any available tax savings but also to ensure and maintain ATO compliance.

A common trap, for example, occurs if the investments funded by way of a debt recycling strategy are subsequently sold. To ensure 100 per cent tax deductibility of the loan is maintained, the amount borrowed to acquire the underlying investment needs to either be repaid or the funds reinvested. Spending the sale proceeds on personal use items while leaving the full loan untouched can reduce the investment use component. Accordingly, one may end up with a lower proportion of tax-deductible interest.

A debt recycling strategy can be highly advantageous in improving an overall tax position through converting private loan interest into tax deductible investment loan interest. There are certainly a few tricks and traps to be mindful of, and the provision of appropriate professional advice will go a long way to ensuring you can maximise potential tax benefits.

Article Q&A

What is debt recycling?

Debt recycling is a financial strategy that involves converting non-deductible debt into deductible debt, potentially reducing tax liability and increasing investment opportunities.

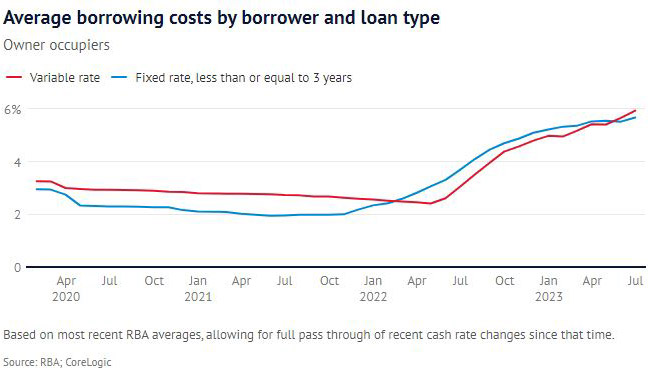

With the mortgage cliff around the halfway point of its gradual transition from low fixed to high variable rate loans, is a looming disaster unfolding or are borrowers proving to be more resilient than expected?

It’s late August and the midway point of what was dubbed the mortgage cliff.

This so-called cliff was named to denote the lemming-like fate that supposedly awaited all who had to move from super low fixed term loans secured from mid-2020 to mid-2022 to loans up to triple that interest rate.

While its progression is far from complete, and much of the impact of this mass switch may still be yet to play out in full, the doomsday scenarios have not eventuated at this stage at least.

There has been a slowdown in economic activity and housing market momentum in response to higher rates across all mortgage holders, while CoreLogic has recorded an unusual increase in new listings over the past few weeks.

But overall, the risk of arrears and default remains contained within Australia’s large mortgage market and a level of resilience demonstrated amid tight labour market conditions.

Property prices have remained resilient for most of 2023 but buyers and sellers alike are eyeing off a crucial spring selling season.

While homeowners are, in broad statistical terms at least, not selling up en masse, they are taking steps beyond trimming the socialising budget to meet these new, sometimes dramatically higher, repayment levels.

The mortgage cliff was all media hype. – Helen Avis, Director of Finance, Specialist Mortgage

The number of Aussie home loan holders refinancing soared 13.8 per cent in the financial year just completed, while those signing new mortgages fell 20.6 per cent, new research from PEXA shows.

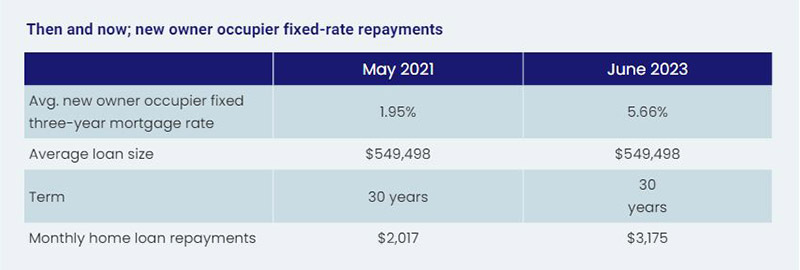

That comes as mortgage holders contend with a transition from interest rates on a loan of around 1.9 to 2.5 per cent leaping to between 6 and 7 per cent.

In terms of what that means to a household’s budget, the repayment on a $750,000 mortgage set at 2 per cent would soar from $3,180 a month to $4,830 a month – an increase of more than 50 per cent overnight, assuming a new rate of 6 per cent.

Yet it seems official data on mortgage stress has not seen a blow out in arrears amid the expiry of low fixed-term loans.

Portion of outstanding loans in arrears

Eliza Owen, Head of Residential Research Australia, said as home values rise, the risk of default also remains low.

“As what is likely to be the last of the RBA’s rate hikes is passed through to households with a mortgage, there may be a mild deterioration in housing market conditions if new listings decisions continue to rise.

“The good news for mortgage holders is that this period of economic slowdown will also take the RBA closer to its long-term inflation target, which could be the impetus for a reduction in the cash rate in the second half of 2024, as predicted by most major banks.”

Whether there is another 0.25 per cent increase in the official cash rate by the RBA is an even money bet. But the governor, Philip Lowe, used the just-released RBA Board Minutes for August to acknowledge the mortgage cliff was a consideration in their decision-making process around interest rates.

“Members noted that banks had continued passing increases in the cash rate through to their customers, and that outstanding mortgage rates and scheduled mortgage payments were set to increase further as a high share of fixed-rate loans roll onto higher rates through the rest of 2023.

“Scheduled mortgage payments as a share of household disposable income increased to 9.4 per cent in the June quarter, around its historical peak.

“Voluntary principal payments into borrowers’ offset and redraw accounts declined in the June quarter (while) net flows into these accounts had declined to be noticeably lower than the pre-pandemic average, consistent with pressures on disposable incomes.”

To be more concise, borrowers are hurting.

Finding more than $1,000 a month for mortgage repayments isn’t easy for everyone.

Climbing or falling from the mortgage cliff?

Industry sources are divided on just how severe the implications of the mortgage cliff’s continued unfolding will become. Some argued it was driven by an excitable media while others declare it’s downward spiral with no imminent escape route.

In the former camp, Helen Avis, Director of Finance at Specialist Mortgage, said “the mortgage cliff was all media hype.”

“I cannot see rates rising too much further, and if that is the case then we should not see much more of an adjustment from where we are at now.

“I am not surprised with the lack of delinquencies, with the still relatively strong property market and borrowers able to handle the increases.

“That said some borrowers have been affected and are struggling but the vast majority seem to be coping.

“I know some first home owners who have rented their property and gone back to live with parents, capitalising on the acutely tight rental market to offset the stress of higher mortgage repayments.”

Joe White, President, Real Estate Institute of Western Australia (REIWA), said we are well into 2023 and we have not seen the apocalypse we were told was coming.

“While there have been constant predictions of a flood of forced sales, REIWA data does not yet show an increase in properties advertised as mortgagee sales or mortgagee in possession.

“There is no denying 12 interest rate increases have had an impact on households, but it is disingenuous to underestimate a homeowner’s capacity and willingness to adjust their spending habits.

“Many homeowners on fixed rate loans have prepared for the dreaded mortgage cliff.

“They have paid extra onto their mortgage to be ahead with their repayments, have created a savings buffer or have refinanced.”

API Magazine’s recently released Property Sentiment Report found that the percentage of respondents defining their situation as being in mortgage or rental stress was easing.

While still disturbingly high at 36 per cent, it was an improvement on the 43 per cent of the previous quarter. Disconcertingly, 79 per cent said their financial stress status had eventuated over the past 12 months.

Mark Bouris, Executive Chairman, Yellow Brick Home Loans, however, was far less optimistic than others, reporting that the consequences of the interest rate hikes won’t be fully laid to bear until Christmas this year, as more and more home loans move from cheap fixed rates to high variable rates.

“Expect families to be forced to sell their homes, many to property investors and foreign buyers, and end up in the already-crowded rental market that is driving up inflation.

“Otherwise, families will be forced to cut back their spending on everything from holidays to food to recreational activities and school fees – the list goes on.

“This will hurt the small businesses that rely on consumer spending to pay their bills, which are also rising.

“It’s a vicious cycle, and there’s no clear way out.”

There has been a sharp spike in landlord exits from the property market across Australia.

Victoria is the worst-hit state, with the latest PropTrack figures revealing 30.1 per cent of sales were properties that had been listed for rent since they were purchased.

That’s up from 24.7 per cent in July 2022, and 16.9 per cent in July 2019, before the pandemic. New South Wales followed at 28 per cent, which like Victoria, was also the state’s highest share of investment home sales since late 2018. Queensland was third with 27.15 per cent of sales in July being rental properties.

Regardless of which side of the fence you sit on in terms of the mortgage cliff’s ultimate impact, the rest of the year promises to offer compelling viewing of the economy, housing market, and the financial viability of renters, home owners and investors alike.

Article Q&A

What is a mortgage cliff?

The mortgage cliff refers to the sudden large increase in repayments mortgage holders on fixed rate loans will face when their term ends and their loans revert to variable, and the subsequent effect this will have on the property market.

What has been the impact of the mortgage cliff?

While its progression is far from complete, the doomsday scenarios of the mortgage cliff have not eventuated at this stage at least. There has been a slowdown in economic activity and housing market momentum in response to higher rates across all mortgage holders, while CoreLogic has recorded an unusual increase in new listings.

Will property prices fall because of the mortgage cliff?

Property prices have remained resilient for most of 2023 but buyers and sellers alike are eyeing off a crucial spring selling season. While homeowners are, in broad statistical terms at least, not selling up en masse because of the mortgage cliff, they are taking steps beyond trimming the socialising budget to meet these new, sometimes dramatically higher, repayment levels.

Barely a quarter of property investors feel in control at tax time, as the ATO ramps up its scrutiny on property investors throughout the end of financial year tax season.

Property investors are feeling the heat from the Australian Taxation Office (ATO), with seven out of ten saying there was more intense scrutiny on them and six out of ten saying recent legislative changes were difficult to navigate.

The ATO is implementing stringent measures that are set to have significant implications for property investors across the country.

Their decision to ramp up their efforts comes in response to a surge in tax return inaccuracies reported in recent years, with property investors found to be one of the major contributors to the problem.

Unintentional mistakes, misinterpretations, and deliberate omissions have resulted in a substantial loss of revenue for the government, leading to the urgent need for stricter enforcement.

Starting from the financial year 2023-2024, the ATO will be deploying advanced data analytics and artificial intelligence tools to conduct comprehensive cross-referencing of taxpayers’ reported income and property-related deductions. This initiative will enable the tax authority to detect anomalies, irregularities and discrepancies in a more efficient and timely manner.

Property investors are being pushed to make financial decisions they may not have considered just 12 months ago.

– Nicole Kelly, Founder, TaxTank

Australasian Taxation Services’ Director, Jason Lawrance, defended the ATO’s new approach, saying it sends a clear message to all taxpayers about the importance of accuracy and integrity in their financial dealings.

“As the ATO’s intensified crackdown takes effect, property investors are advised to take extra caution when preparing their tax returns.

“Seeking guidance from qualified tax professionals and diligently documenting all relevant income and deductions will be crucial in avoiding potential pitfalls and ensuring compliance with tax laws.”

He acknowledged concerns raised by critics who argue the ATO must ensure that its artificial intelligence and data analytics tools are error-free and capable of distinguishing genuine mistakes from deliberate tax evasion attempts.

“Ultimately though, the ATO is less concerned with intent than it is with accuracy, so the onus is on property investors to get it right, even if it is a complicated process, to avoid facing the ATO’s increased scrutiny as a result of the crackdown,” Mr Lawrance said.

Taxing time for property investors

Recent research conducted by TaxTank at the end of financial year tax season found that only around one in four property investors felt comfortable with the tax return process.

It found that most property investors (71 per cent) are concerned about missing out on possible deductions, and more than half (57 per cent) are concerned about making a mistake. Recent legislative changes were difficult to navigate according to 59 per cent of respondents.

A mere 27 per cent of property investors feel ‘in control’ at tax time.

Nicole Kelly, Founder of TaxTank, said the increased power given to the ATO and their intensified scrutiny of property investors is creating significant concern and stress.

“For millions of taxpayers across Australia, they are merely trying to navigate the tax system in a way that delivers compliant, legal, fair, and accurate outcomes for both sides, however, with changing regulation and the looming threats made by the ATO, many investors end up putting their taxes in the ‘too hard basket’ before they have even started the process.

“This scrutiny also increases the pressure on agents, which further exacerbates the cost of compliance on individuals.”

The ATO has also warned the public of schemes aiming to tempt SMSF trustees into illegal early release arrangements or inappropriately channelling money or assets into an SMSF to pay less tax.

Interest rates putting pressure on investors

The TaxTank research also revealed that 78 per cent of property investors have been impacted by interest rate rises, with more than half (54 per cent) needing to take action to manage repayments. This includes 32 per cent increasing the rent of their property, 15 per cent refinancing, 15 per cent pursuing a higher income, and 7 per cent selling their property.

Uncertainty about the future of the property market and interest rates is also impacting property investors.

Most property investors (78 per cent) believe interest rates will continue to rise and more than one in five (22 per cent) expect them to continue to rise for the foreseeable future. Almost half (45 per cent) feel uncertain about the future due to higher interest rates.

“Property investors are navigating a fast-moving and constantly changing property landscape at the moment and are being pushed to make financial decisions they may not have considered just 12 months ago,” Ms Kelly said.

“This is putting many taxpayers in a difficult situation, where they need to simultaneously weigh up the pros and cons of managing a property with the realities of needing to pay larger monthly bills amid an uncertain economic backdrop.”

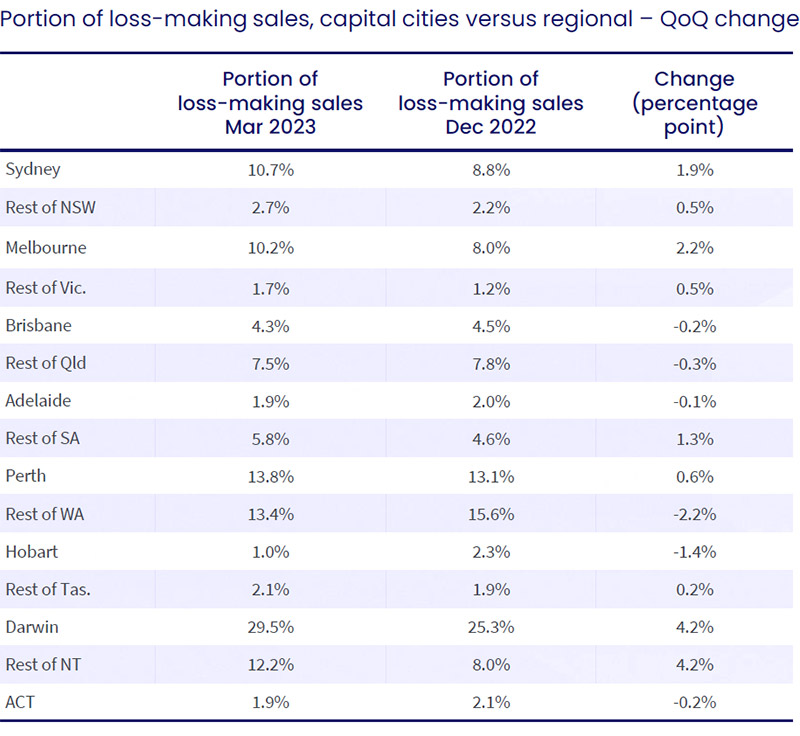

Inflation is easing just as property sales around the country are becoming less profitable but one state stands out when it comes to attracting buyer interest.

When it comes to the proportion of property sales making a loss Western Australia is hurting more than other states, while buyers seem transfixed on the Victorian property market.

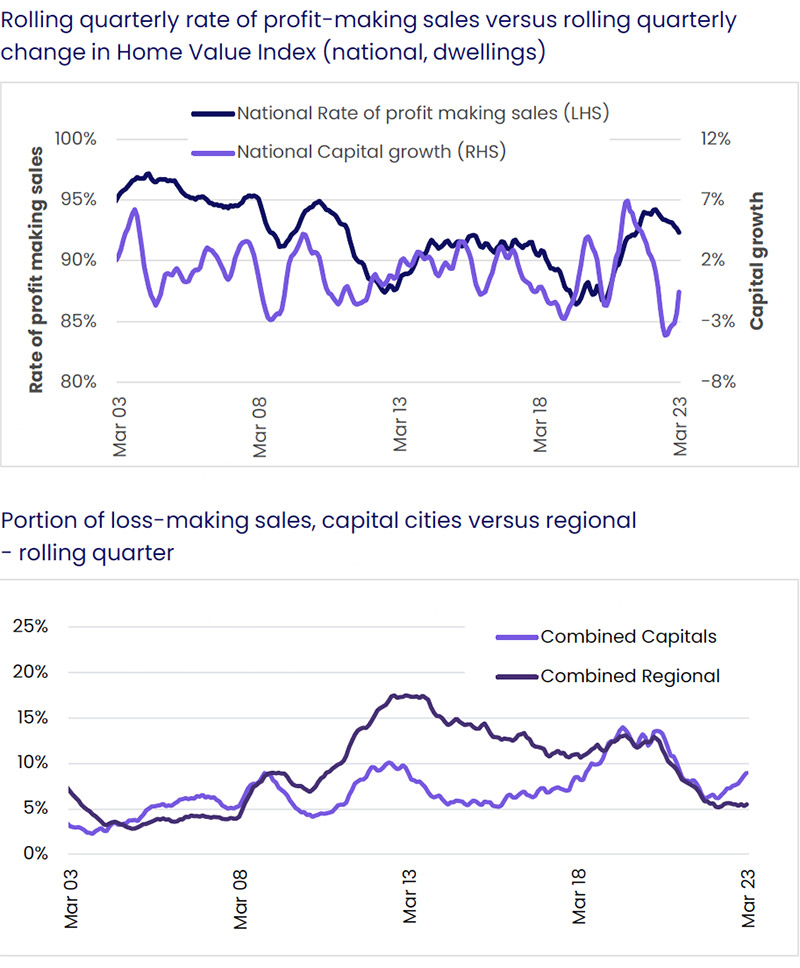

For the third consecutive quarter the rate of profit-making resales around the country has dropped, although this week’s fall in inflation may offer hope of a turnaround down the track.

While there’s no sign in the market yet of panic selling, indications are emerging that some property owners are willingly selling at a loss to avoid rising mortgage interest repayments.

According to CoreLogic’s Pain and Gain Report June 2023, the rate of lossmaking sales was most concerning in the unit market, while Darwin and Perth had the most disgruntled sellers accepting a loss on their property investment.

The rate of loss-making sales nationally across the house market increased by 20 basis points to 3.8 per cent in the March quarter, but the share of loss-making unit resales jumped to 15.4 per cent from 13.8 per cent in the previous quarter.

Source: Corelogic.

Of the capital city markets, the rate of profit-making sales was highest in Hobart, where 99.0 per cent of resales made a nominal gain. This was followed by a rate of 98.1 per cent across Canberra and Adelaide.

At the other end of the spectrum, Darwin, Perth, Sydney and Melbourne saw increases in the rate of loss-making sales to relatively high levels.

In Sydney, the incidence of loss-making sales reached 10.7 per cent in the March quarter, its highest level since the three months to August 2009. The Brisbane housing market saw a slight increase in the rate of profit-making sales, to 95.7 per cent in the quarter.

Property buyers keen on Victoria

Around one in ten Melbourne sellers may have sold at a loss but that hasn’t tempered the flood of enquiries and buyer interest in the Victorian capital and some of its scenic regional areas.

Winter is typically a quieter season for the property market but clearance rates in June were higher than the lows seen late last year, and auction volumes are staying in line with last year’s levels.

New data from PropTrack has revealed the most in demand suburbs this winter, based on the most highly engaged people for houses listed on realestate.com.au in the past year.

Anne Flaherty, Economist, PropTrack, said Victoria is seeing the highest level of engagement of any state, particularly among those looking to purchase a house.

“Victoria accounted for nine of the top 10 most highly engaged suburbs for houses and six of the top 10 for units.

“Suburbs seeing the most engagement among those looking to buy a house are typically located in middle and outer metropolitan areas of capital cities.

When it comes to the suburbs seeing the highest level of engagement for units, inner city areas dominate, with the Melbourne, Brisbane, and Adelaide central business districts all making the national top 10.”

Source: Corelogic.

“Across all states, the suburbs seeing the most engagement from buyers are typically located in scenic areas that combine high levels of liveability with excellent amenity.

“Standout regions include Sydney’s scenic Northwest, Melbourne’s Outer East and Mornington Peninsula, and Queensland’s Gold Coast,” Ms Flaherty said.

Julie Kelley, Global Sales and Marketing Manager for aussieproperty.com, said the country is experiencing an influx of new residents and an increase in new buyers who are transitioning from renting – buoyed by the fact that in some cases purchasing a home is more affordable than renting.

“While we welcome 1,361 people day to Australia our housing market is unable to cope.

“According to Domain, Australia will require an additional 487,984 homes in the next four years to house 1,235,000 net oversees migrants, equating to 341 new homes every day for four years.

“Given this, I believe it’s realistic to predict the Australian housing crisis will worsen, driving housing and rental prices up with increased demand,” Ms Kelley said.

Will falling inflation quell interest, hit sales profitability?

Inflation may at last be responding to more than a year of interest rate hikes, with Australia’s Monthly Consumer Price Index (CPI) Indicator dropping to an annual rate of 5.6 per cent for May, down from 6.8 per cent recorded in the previous month.

This significant figure, released by the Australian Bureau of Statistics on Wednesday (28 June), represents the smallest annual increase since April 2022 and came in well below market expectations of 6.1 per cent.

If the Reserve Bank of Australia (RBA) sees this as a plausible reason to hit pause on interest rates, the proportion of sales expected to be made at a loss over the coming year could decline appreciably as distressed sales abate.

Of concern to borrowers and potential buyers will be the hidden detail in that inflation figure.

While the likes of the Real Estate Institute of Australia are saying the RBA should stop rate rises indefinitely in response to this latest ABS data, the RBA may be less convinced.

The lower CPI figure was largely driven by items volatile price changes, like fuel, fruit and vegetables and holiday travel. When these factors are stripped out, the decline in inflation was more modest, landing at 6.4 per cent, a drop of just 0.1 per cent.

Shane Oliver, Head of Investment Strategy and Economics and Chief Economist, AMP Investments, said the risk of recession globally and in Australia has increased with ongoing central bank rate hikes.

“Australian home prices have rebounded from their lows as a severe supply shortfall has dominated rising rates, however, a recession could drive another leg down in home prices as buyers back off, higher rates and higher unemployment push up distressed selling, and recession drives reduced household formation,” he said.

“CoreLogic data shows a 9 per cent fall in capital city property prices in the early 1980s recession with a 25 per cent fall in Sydney, and a 6 per cent fall in the early 1990s recession with a 10 per cent fall in Sydney.”

Time, and the RBA, will tell if this pays out as continued increases in sales made at a loss and a decline in interest in property investment.

Article Q&A

Are properties selling for a profit in Australia?

For the third consecutive quarter, the rate of profit-making resales around the country has dropped, with units hit hardest. The rate of loss-making sales nationally across the house market increased by 20 basis points to 3.8 per cent in the March quarter, but the share of loss-making unit resales jumped to 15.4 per cent from 13.8 per cent in the previous quarter.

Where are property buyers looking in Australia?

New data from PropTrack has revealed the most in demand suburbs this winter, based on the most highly engaged people for houses listed on realestate.com.au in the past year. Victoria has accounted for nine of the top 10 most highly engaged suburbs for houses and six of the top 10 for units.

What is the inflation rate in Australia?

Inflation may at last be responding to more than a year of interest rate hikes, with Australia’s Monthly Consumer Price Index (CPI) Indicator dropping to an annual rate of 5.6 per cent for May 2023, down from 6.8 per cent recorded in the previous month.

Melbourne property prices have failed to keep pace with Sydney and other capital cities since Covid but the Victorian capital may be poised to strike back as a property investment prospect.

It may take around 40 years to pay off a home on the average salary in both cities, but that isn’t enough to stifle a Sydney-Melbourne rivalry that transcends sport and culture to include their respective property markets.

In a rivalry that purportedly dates back to the to 1871 when the very first intervarsity competitions in Australia were a boat race and cricket match between their two great universities, Melbourne won both inaugural events.

Sydney had long been the most populous city but that recently changed too when Melbourne was this year deemed to have overtaken the Harbour City.

But when it comes to property prices, Sydney’s mantle as the priciest real estate remains unchallenged and it is seemingly extending its lead over its southern neighbour.

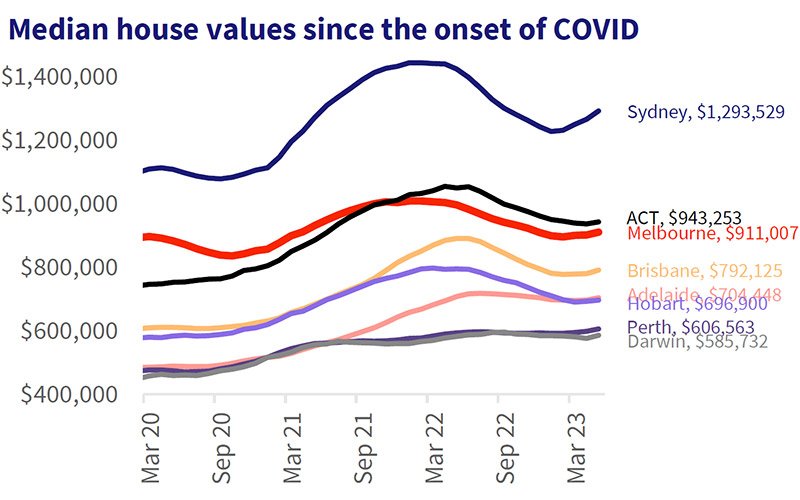

Property prices since the onset of Covid have seen the two cities take divergent paths.

Source: CoreLogic

Melbourne house values have increased a mere 1.6 per cent between March 2020 and the end of May 2023. Every other capital city has seen double-digit growth, ranging from a 16.5 per cent gain in Sydney to a 45.2 per cent surge in Adelaide house values during that period.

But while Melbourne may be lagging the New South Wales capital, investors could be licking their lips at the prospect of investing in a city with high population growth and relative affordability compared to Sydney.

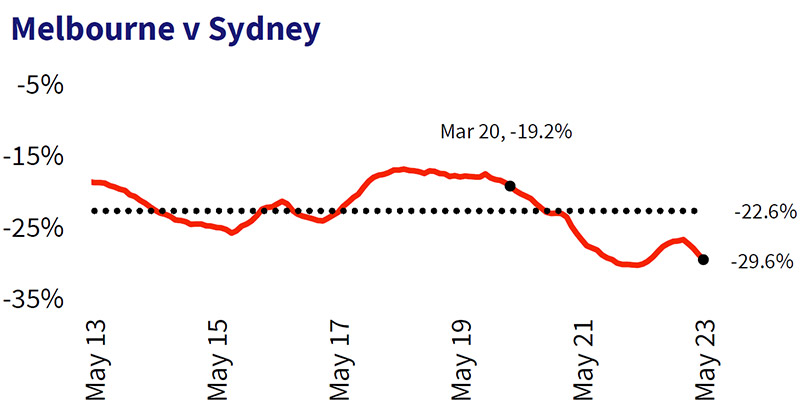

According to CoreLogic, at the onset of Covid Melbourne house values were 19.2 per cent cheaper than Sydney’s. By April 2022 the gap between Sydney and Melbourne house values had blown out to 30.3 per cent, the biggest divergence since May 2006.

The gap has closed a little since then however Melbourne’s median house value was 29.6 per cent behind Sydney’s in May 2023, the dollar equivalent of $382,500.

Every capital city other than Canberra – the country’s second most expensive capital for houses – has significantly closed the house value gap to Melbourne. At the onset of the pandemic, Brisbane houses were 47 per cent cheaper than Melbourne. That affordability gap has closed to just 15 per cent.

Melbourne vs

Difference in median house value – March 2020

Difference in median house value – May 2023

$ difference with Melbourne – May 2023

Sydney

-19.2%

-29.6%

$382,500

Canberra

20.1%

-3.4%

$32,200

Brisbane

47%

15%

-$118,900

Adelaide

85%

29.3%

-$206,600

Perth

88.2%

50.2%

-$304,400

Hobart

54.5%

30.7%

-$214,100

Darwin

95.7%

55.5%

-$325,300

Tim Lawless, Research Director, CoreLogic Asia Pacific, said Melbourne may still have a competitive edge in terms of future capital growth performance.

“With housing affordability remaining stretched, this improvement in Melbourne’s value proposition could place the city in a more competitive position to attract a greater share of housing market participants.

“The city’s advertised supply level is trending lower and is 13.4 per cent below levels at the same time last year and 7.0 per cent below the previous five-year average.

“Melbourne’s rental vacancy rate of 0.8 per cent in May is also one of the lowest in the country and yet another potential factor supporting purchasing demand for those with the financial capacity to enter the market,” Mr Lawless said.

He did add however that the outlook wasn’t necessarily as smooth as an MCG cricket pitch on Boxing Day.

“Whether Melbourne’s strong demand, low supply and a relative affordability advantage can completely offset the impact of high interest rates remains uncertain,” he said.

“Demand from overseas migration is likely to remain a feature of the market for the next few years, however, borrowers’ access to credit will be challenging while interest rates are high.”

Melbourne was 85 per cent more expensive than Adelaide at the start of Covid but the gap has narrowed to just 29 per cent and in Perth, where the gap was 88 per cent, Melbourne house values are now 50 per cent higher.

Source: CoreLogic

Melbourne’s softer housing market conditions through the pandemic cycle coincided with a sharp drop off in demographic trends, according to Mr Lawless.

Both net overseas and interstate migration rates fell sharply through the pandemic, reaching record lows, detracting from housing demand amid a series of lockdowns associated with the pandemic.

“Demographic data to September 2022 shows Victoria’s interstate migration is normalising and was almost back in positive territory (-484 net interstate migrants).

“With demographic data for Q4 2022 to be released soon, it’s likely Victoria will be once again have reached a positive interstate migration position, putting an end to 10 consecutive quarters of decline.

“With Australia’s annual net overseas migration surging to new record highs and Victoria’s first possible rise in interstate migration since Q1 2020, housing demand across Melbourne has begun to strengthen substantially.”

Steve Janes, Melbourne-based property consultant for aussieproperty.com, said he expected the next year or two to deliver strong growth in Melbourne’s apartment sector and within the CBD due to investors seeking the higher rental yields on offer and surging migration.

“The recent upward trend in overseas migration back into Melbourne has the potential to further bolster the apartment sector, particularly considering the prevailing challenges faced by construction projects across the state.

“With more people choosing Melbourne as their destination, there is an increased demand for housing, including apartments in the inner city, however, the supply of new apartments is likely to be constrained due to disruptions in supply chains and builder insolvencies impacting construction projects across the state.

“This limited supply, coupled with the growing demand from incoming migrants, can potentially drive up the value and desirability of existing apartments.

“Investors may find this trend advantageous as they can capitalise on the potential for price appreciation and rental income, given the restricted availability of new construction projects,” Mr Janes said.

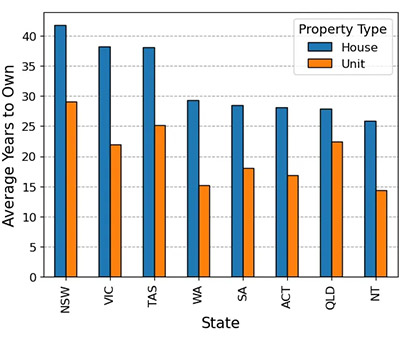

New research from Proptech platform HtAG Analytics found that housing affordability has continued to decline, with the number of years it takes to pay off and own a property in Sydney and Melbourne ballooning to 40 years.

Alex Fedoseev, Co-founder, HtAG Analytics

Their analysis was based on the number of years it would take a homebuyer to fully repay their home loan based on median home prices and median family income levels in their suburb of residence.

Sydney suburb Strathfield was in a league of its own as the least affordable suburb in the country based on income levels, requiring an astonishing 140 years to pay off based on residents’ current income levels.

New South Wales was found to be the country’s most unaffordable housing market, taking on average 42 years to pay off a free-standing house based on the median family income.

Victoria was second at 39 years and Tasmania third at 38 years. All the major capital cities required a mortgage holder to spend 25 to 30 years paying off a mortgage.

For units, Soldiers Point in northern NSW (82 years to own), Noosa Heads in Queensland (75 years) and Byron Bay in NSW (74 years) proved to be the most unaffordable markets.

While they may be rivals, Sydney and Melbourne had much in common.

HtAG Analytics co-founder, Alex Fedoseev said the two cities’ property markets have now reached an unaffordable level compared to the rest of the country.

“In states like South Australia and Queensland, the gap between owning a house and a unit is relatively smaller, indicating a more balanced property market,” Mr Fedoseev said.

“In contrast, New South Wales and Victoria exhibit a larger disparity, demonstrating the dominance of higher-priced houses in those markets.”

Mr Fedoseev said two common factors contribute to the consistent unaffordability of suburbs with years to own above 100, namely high house prices coupled with a prevalence of renters or exclusive locations with generational wealth.

“In these markets, a significant portion of the population is engaged in renting units rather than owning a house,” he said.

“While the majority of household incomes in these suburbs may suffice for renting or owning a unit, they may not be adequate for purchasing houses.

“This leads to a property market that primarily supports rental properties in units and maintains high house prices.”

Article Q&A

Does Sydney or Melbourne have the better performing property market?

When it comes to property prices, Sydney’s mantle as the priciest real estate remains unchallenged and is seemingly extending its lead over its southern neighbour. Melbourne’s median house value is 29.6 per cent behind Sydney’s, the dollar equivalent of roughly $382,500.

How has the Australian property market performed since Covid?

Melbourne house values have increased a mere 1.6 per cent between March 2020 and the end of May 2023. Every other capital city has seen double-digit growth, ranging from a 16.5 per cent gain in Sydney to a 45.2 per cent surge in Adelaide house values during that period.

How long does it take to pay off a house?

New research has found that housing affordability has continued to decline, with the number of years it takes to pay off and own a property in Sydney and Melbourne ballooning to 40 years based on the average income within the suburbs examined..

Property investors have been deterred from investing in Melbourne by myriad government policy obstacles but segments of the market are ripe for investment.

Melbourne’s tight property market is as unpredictable as any in Australia right now but real estate experts are adamant golden opportunities exist despite misguided government policy unnecessarily poisoning the lawn for investors.

Despite economic and policy pressures, Andrew Meehan, President, Real Estate Institute Victoria (REIV), is confident there are buying and selling opportunities

“We expect to see this stability continue into the second half of the year,” he said.

Melbourne units delivering the capital growth

REIV released quarterly median data this week showing Melbourne units have climbed 3.2 per cent to $630,500.

The highest quarterly growth was seen in units in the eastern suburb of Mount Waverley, which climbed almost 25 per cent to $1,245,000. Million-dollar units in bayside suburbs climbed even higher, with Hampton units rising 20.1 percent to $1,105,000 and Brighton East increasing 14.9 per cent to $1,402,500.

Steve Janes, Buyers Agent, aussieproperty.com

Steve Janes, Melbourne-based property consultant for aussieproperty.com, says he’s on the record as being anti-apartment but says the growth is significant.

“I believe we are in the middle of a unique apartment bubble, whereby I’m seeing up to 10 per cent growth in the one and two-bedroom apartment space.

“That is coming from a very low base and primarily driven by the rental crisis, given that first home buyers who would normally sit on the fence and not buy don’t really have a choice at the moment.

“I think the one number that’s really important is occupancy; it’s a record low pretty much across the world right now but 0.8 per cent is incredibly low and I think it’s an absolutely golden to sell because if this market does slow down, unemployment goes up, and more pressure does come then that icing on the cake will disappear immediately in the apartment sector.

“A lot of investors have been waiting 10-15 years, waiting for some hope of recovery, and I believe this window is exactly that,” Mr Janes said.

Houses prices rebounding Victorian capital

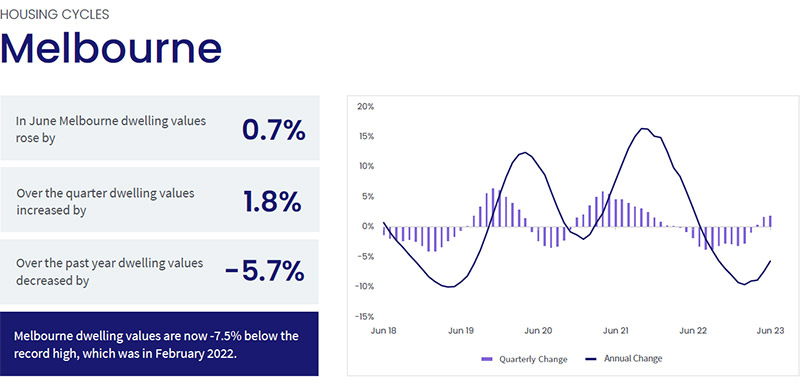

Melbourne house prices rebounded in the last quarter by 1.8 per cent, still 7.5 per cent below the city’s record high set in February 2022 and sluggish compared to Sydney where quarterly values rose 4.9 per cent, Brisbane 3 per cent and Perth 2.8 per cent, according to CoreLogic.

Middle Melbourne suburbs are excelling according to REIV data, such as Mulgrave which grew 17 per cent from $970,000 to $1,135,000, a trend also seen in Patterson Lakes ($1,116,000 from $865,000), Sandhurst ($1,100,050 from $965,500), Knoxfield ($1,080,500 from $862,500) and Heidelberg Heights ($1,032,500 from $905,000).

“Nobody’s really quite sure what is going on, we’re all expecting a bit of a slowdown but the ones I’m buying in that premium middle market, between $1- and $2 million-dollar houses, they’re flying, whether buying or selling,” Mr Janes said.

Homes in the inner suburbs of Kew and Malvern recorded quarterly declines in median house prices of more than 9 per cent to $2,900,000 and $2,775,000 respectively while in outer Melbourne, Melton South houses sit at $460,000 (down 2.4 per cent), and Harkness at $570,000 (down 3.4 per cent).

Ben Kingsley, Chair, Property Investors Council of Australia, said the biggest challenge confronted the bottom quartile, as people try to juggle their mortgage repayments and the family budget.

Source: Corelogic.

“With high interest rates, demand in these locations experiences a downturn while the upper quartile has experienced the most growth (+2.1 per cent) over the past quarter, as higher income earners aren’t as impacted, and with very limited quality of stock they are competing harder to secure properties in the upper end of the market.”

Government policy punishing investors

Michelle Stephens, real estate agent with O’Brien Real Estate in Carrum Downs, located south of Dandenong and 40 minutes’ drive from Melbourne’s CBD, said investors are currently thin on the ground despite Melbourne offering affordable investment opportunities.

“Investors are hamstrung by legislation around rent increases in Victoria so that has played a part in this, and government policy is making it very difficult on investors and for new builds to get through with all the red tape.”

Ben Kingsley, Chair, Property Investors Council of Australia

Mr Kingsley described Melbourne as experiencing a boycott of investors, which he says was initially triggered by tenancy reforms that included 133 new amendments introduced in March 2021 that scared off investors.

“Then, the recently introduced increases to land tax, as part of the new Covid levy, has made Victoria the most expensively property taxed state in the country, according to the Parliamentary Budget Office, and far less attractive for investors, so they are looking elsewhere for their opportunities.

“Investors don’t trust the government to give them a fair go, so that buying group is taking its investment dollars elsewhere, especially with rumours circling that the Andrew’s Government is considering rental caps or freezes, which would kill off new investment into Melbourne and see a lot of investors selling up.

“Not being able to recover interest rate rise costs will mean some mum and dad investors will be forced to sell, and with other budding property investors snubbing Victoria because it’s too hard and too costly to hold properties, the story is going to be pretty dire for the state and for all renters living there.”

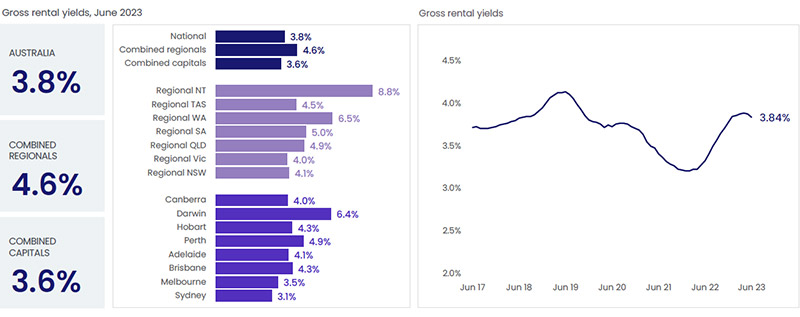

Rents up but yields still low

Melbourne’s rental growth remains well above average with rents up 12.6 per cent on the same time last year.

The city and has shown the strongest quarterly growth (3.9 per cent) of all capitals, where Perth was 3.4 per cent, Sydney (3.2), Adelaide (2.5) and Brisbane (2.1), while both Canberra and Hobart saw rents fall 1 per cent.

According to CoreLogic’s June Quarterly Rental Review, Melbourne lost its position as the country’s most affordable rental capital for houses over the three months to June with an average of $567 p/w, behind Hobart averaging $565 p/w.

Source: Corelogic.

Melbourne’s gross rent yield in June was one of the lowest in the nation at 3.5 per cent, compared to Darwin (6.4 per cent), Perth (4.9 per cent), Brisbane and Hobart (4.3 per cent), Adelaide (4.1 per cent) and the poorest performer, Sydney (3.1 per cent).

“Rental yields are actually going to be the only real positive property story for Melbourne, with vacancy rates sitting at 0.8 per cent and in the past month rents in Melbourne increased faster than any other state as it heads into a period of chronic undersupply of rental accommodation,” Mr Kingsley said.

“This will push rents higher and improve rental yield over the next couple of years if values remain steady.”

Busy auction market

Melbourne listings were down in June compared to the same time last year by 5.5 per cent (Sydney down 3.1 per cent), but both cities fare better compared to Brisbane (-25.0 per cent), Hobart (-29.9 per cent), Perth (-18.7 per cent), Adelaide (-21.4 per cent) and Canberra (-16.8 per cent).

Michelle Stephens, O’Brien Real Estate, Carrum Downs, Victoria

Last weekend, Melbourne was the busiest auction market with 566 homes scheduled for auction across the city, down five auctions from the previous weekend and down 16.1 per cent on auctions held the same week last year. There was just one auction difference between Melbourne and Sydney.

“The context here is that 12 months earlier, Melbourne listings were lower than other states, so although new listings are down only 5.5 per cent year-on-year, and total listings are down 12.4 per cent year-on-year, Melbourne’s overall listings during and just after the Covid period haven’t really returned to normal listing levels compared to other states and territories, meaning they have been lower for some time, not just compared to the past 12 months,” Mr Kingsley said.

Based on agent reports, REIV auction sales and results from last Saturday (15 July) showed a clearance rate of 78 per cent from 387 auctions held, down from the previous week’s 491 properties on auction and 502 from the same time last year.

Ms Stephens agrees the pricing is strong despite the lack of properties.

“Sandhurst is a suburb that has gone against the trend and has seen price growth in the last 12 months,” Ms Stephens said.

Article Q&A

What is the median apartment price in Melbourne?

REIV released quarterly median data showing Melbourne units have climbed 3.2 per cent to $630,500.

What is the median house price in Melbourne?

Melbourne house prices rebounded in the last quarter by 1.8 per cent, still 7.5 per cent below the city’s record high set in February 2022 and sluggish compared to Sydney where quarterly values rose 4.9 per cent, Brisbane 3 per cent and Perth 2.8 per cent, according to CoreLogic.

Where are rental yields highest in Australia?

Among Australia’s capital cities, Melbourne’s gross rent yield in June was one of the lowest in the nation at 3.5 per cent, compared to Darwin (6.4 per cent), Perth (4.9 per cent), Brisbane and Hobart (4.3 per cent), Adelaide (4.1 per cent) and the poorest performer, Sydney (3.1 per cent).

There are two main facilities on a family home loan that should exist in anyone’s tax planning toolbox but unfortunately, they are often misunderstood or improperly used.

There are two main facilities on a family home loan that should exist in anyone’s tax planning toolbox. Unfortunately, they are often misunderstood or improperly used.

Variable home loans are generally more likely to offer features like an offset account or a redraw facility, which are two alternative options that help homeowners reduce their mortgage repayments.

Both tools have contributed to the record rate of debt repayments seen across the country.

Bankwest, for example, said that in March 2022, more than 90 per cent of customers were ahead on their home loan repayments. The average months by which customers were ahead (around three years), increased by 45 per cent.

Their data showed a huge uplift in the volume of savings put into home loan offset accounts. From June 2019 to March 2022, offset account balances grew by 63 per cent – nearly triple the rate of personal savings growth for the period of 23 per cent.

The surge in home loan repayments was matched by a rapid uptake in new home loan offset accounts linked to an eligible home loan, enabling households to use existing savings to reduce their current home loan balance.

Comparison researchers Canstar found that all variable rate home loans and a majority (61.7 per cent) of fixed rate home loans offer a redraw facility.

Canstar analysis of the owner-occupier and investment home loans found that the vast majority of variable rate loans (93.7 per cent) – along with over one-third of fixed rate loans (35 per cent) – offer a full offset account.

So, what exactly are these two, often misunderstood but common, home loan features?

Offset account

This is a standard bank account that is linked to your loan account. The offset account will normally be with the same financial institution as the mortgage provider.

The offset account effectively reduces the loan balance by the amount of money in the offset account, thus reducing the interest component on the monthly loan repayment. This only works with variable rate loans, not fixed rate loans.

This is an ideal location for your emergency cash-float and where your salary or income should be deposited.

The money in an offset account is technically your money, not the bank’s or an early loan repayment. This means that if you take money from the offset account to buy an income producing asset like shares, the interest charged on that purchase cannot be claimed in your tax return.

Purchasing investment assets in this way keeps the loan with its original use, being the family home, not the new asset purchase and the interest not a tax deduction.

So, the main benefit of an offset account compared to an ordinary transaction account is that the money you put into it is ‘offset’ daily against the balance of your home loan, and interest is charged against this reduced amount, rather than the full outstanding balance of your home loan.

Redraw facility

The redraw facility provides the ability to pay down your home loan mortgage in advance and at any time while the loan is active, and then withdraw some or all the amounts paid in advanced.

The act of redrawing alters the usage of the withdrawn amount into a new loan, secured against the family home but assigned to its next use.

If the next use of that money is to generate taxable income, then the interest cost on that new loan (redrawn) amount is tax deductible and ‘good debt’.

If the redrawn amount was used to buy a boat or go on a family holiday, which do not produce taxable income, then the interest cost on this new loan is not tax deductible, and the new loan is considered ‘bad debt’.

The family home, or as we like to refer to it, ‘The Lazy Uncle’, can utilise the redraw facility to maximum advantage.

This works during periods of low interest rates where the cost of borrowing is less than what can be earned by investing in tax advantaged assets, like Australian shares, investment properties or interest-bearing investments, such as fixed interest bonds.

By using the redraw facility and structuring the new loans into sections of variable and multi-year fixed rates for peace of mind and repayment stability, a tax planning strategy starts to emerge where additional cashflow produced can help with:

accelerated reduction of the family home loan

additional income to support living expenses

additional superannuation contributions.

When it comes to funding early, semi or full retirement, using the redraw facility and putting the ‘The Lazy Uncle’ to work is an effective tax planning strategy to consider well in advance of leaving full employment or paying off the family home loan too soon.

Offset account or one-off lump sum repayment into a redraw facility: impact with a $500,000 loan at 3% over 30 years

Offset/redraw amount at start of loan

Total interest paid over life of loan

Interest saved

$0

$258,887

–

$5,000

$251,677

$7,210

$10,000

$244,640

$14,247

$20,000

$231,070

$27,817

Source: Canstar. Based on a $500,000 loan with an interest rate of 3%, repaid over 30 years with principal & interest repayments. It is assumed that the offset account balance is kept constant at the specified amount for the entire loan term, or alternatively that the lump sum repayment of the specified amount is made at the start of the loan. Calculations do not take into account any fees that may apply.

Regardless of which strategy is adopted, any extra money paid off on a mortgage or kept in an offset account could save a significant amount in interest in the long run.

But features such as an offset account or redraw facility, as well as refinancing in pursuit of a better deal, can also add costs to a home loan in the form of additional fees or a higher interest rate and may have tax implications, so it’s always worth seeking professional advice to identify the best approach.

With research and patience, subdividing land can provide property investors with significant returns while also addressing housing affordability and supply issues.

Subdividing land for infill developments in suburbia is lauded as one solution to alleviating affordable housing undersupply and also presents an opportunity for investors.

Though not without barriers, typically due to government regulations, infill sites do offer positives, such as having water, electricity and internet, already connected.

Property investor benefits

“Many people have trepidation about building and investing in today’s market, with interest rates and inflation figures rising, but we know inflation is going to be high, so as long as interest rates are lower than the inflation rate, you’re still going to be in front,” Summit Development’s Senior Development Consultant, Ewan McConnell, said.

Summit Development Consultants Ewan McConnell, Adrian Johnson and Quentin Lau.

“The bigger picture is that Perth is still undervalued and other markets are starting to muscle in, which is why we strongly encourage our clients to consider a subdividable build-to-rent strategy, as you have the benefits of tax deductions, depreciation, compounding capital growth and rental income that could be paying off your repayments,” Mr McConnell said.

“Given these factors, it’s easy to see why Perth’s property market has been drawing the attention of astute property investors.

“Property is not a speculated, short-term investment, it’s a long-term, stable growth strategy and investors have the potential to maximise their potential and make the most of historically low vacancy rates.”

Perth’s premier rezoned target suburbs

Quentin Lau, Senior Development Consultant, Summit Developments, said investors in Perth infill areas should consider proximity to Perth’s CBD and infrastructure or proposed activity centres such as universities, hospitals, shopping centres and public transport.

“Generally, blue-chip suburbs are going to give you the best return on investment,” Mr Lau said.

A Perth duplex called Kardinya is 747m2 with two single storey, 4×2 homes with theatre rooms. After purchasing the development site the client sought to achieve two street front homes to the 18.5m wide duplex site.

“Areas such as Cannington, Beckenham, Gosnells, Kelmscott, Maddington and Armadale tend to have higher development costs in relation to site soil conditions and drainage requirements and, therefore, are not always favourable for developers.”

Melbourne’s top tip subdivision suburbs

Well before the fluid property climate of the 2020s, the Office of the Victorian Government Architect (OVGA) and Monash Architecture Studio (MAS) released in 2011, the Infill Opportunities report, based on research by MAS, Swinburne University and RMIT University for the Australian Housing and Urban Research Institute (AHURI).

Key findings included strategic locations for infill redevelopments in Melbourne’s middle suburbs being identified as within a seven to 25 kilometre radius of the CBD, being suburbs developed between 1950-1970s, having close proximity to public transport and being outside areas with heritage overlays.

“Selection of lots by their width and depth, as opposed to lot area, is a more effective method of determining suitable development sites.

Common lot sizes in the middle suburbs range from 15-16m in width and 38-43m in depth,” the report suggests.

Long-term subdivision benefits

“Adding value via subdivision is, over the long term, a powerful and relatively safe option worth considering,” Steve Janes, an aussieproperty.com licensed real estate agent, said.

“I’m a huge advocate for engineering one residential home into two or three properties,” he said.

“Of course, subdivision isn’t without its challenges and the process can be complex, expensive, and time consuming, however, the accelerated uplift in capital value will over the medium term increasingly eliminate risk.

“This is despite what you initially pay for the property, within reason of course.

Steve Janes, Licensed Real Estate Agent, aussieproperty.com

“Also known as land banking, the strategy leans on maximising future profit by securing today’s land price.

From the purchase date (day the purchase contract is signed) the end development value shall appreciate at a greater dollar value than a single dwelling (without development prospect) of the same value,” Mr Janes said.

“Indeed, conditional on project delivery, the compounding effect is significant and is the main vehicle for above average performance.”

Over time, uplift in land value can contribute toward construction funding and development completion, activating the tax efficiency of a brand-new investment property.

“In the long term, you can benefit from a diversified portfolio with two or more properties while having only paid one stamp duty.

“Subdivision can be a good property strategy for those looking to create value in a property, maximize its potential use, or invest in real estate,” he said.

Subdivision and housing affordability

Urban Development Institute of Australia National (UDIA) President Max Shifman says it is the right time for bold initiatives that bring all property providers together and bolster land supply to resolve the affordable and social housing shortages.

He acknowledges the Federal Government’s new National Housing Supply and Affordability Council Bill (HAFF) as a ‘golden opportunity’ for government, community housing and private providers to pull together to resolve these shortages.

“We now face the stark reality that Australia needs 45,000 new affordable and social housing each year just to keep pace, yet we are only managing around 8,500 dwellings through government and Community Housing Providers,” Mr Shifman said.

“The decades long decline in new housing supply is a result of a lack of development-ready land due to a lack of enabling infrastructure, increasing cost imposts and inefficient planning processes.

“In addition, up to 60 per cent of zoned housing land is prevented from being built on because of straightforward issues.

“The result is that it can take six years or more to finish building a new house because of planning and approvals,” he said.

Barriers to successfully subdividing

The Victorian Infill Opportunities research demonstrates a range of design strategies for improving the density, quality and performance of small-scale infill housing and identifies the existing planning controls and industry trends incongruous with achieving better redevelopment outcomes.

Current barriers include regulated building setbacks that limit the potential and restrict optimum use of typical suburban sites, plus a growing demand for ensuites to all bedrooms and an expectation of double garages integrated with a dwelling structure are challenge for well designed, smaller infill housing proposals.

A new barrier for Victorians is the recent state government announcement that it would not allow landowners and developers to claim deductions for the costs of rezoning land under its incoming Windfall Gains Tax.

Developers and landowners in Victoria will be subject to the new tax at the rate of 50 per cent of any value gain of more than $100,000 that occurs when land is rezoned, from 1 July.

Craig Whatman, Executive Director Tax Advisory Group, Pitcher Partners.

Craig Whatman, Executive Director Tax Advisory Group, Pitcher Partners, said not allowing developers to claim deductions for pre-rezoning costs would increase the price of house and land packages and act as a deterrent to development activity.

“It had been hoped that the Treasurer would use the power prescribed by the Windfall Gains Tax legislation to allow for deductions to cover a range of costs ordinarily incurred by landowners and developers in the lead up to a rezoning decision,” Mr Whatman said.

“Many of these costs are incurred as a result of requirements imposed by local and state governments as well as other regulatory bodies and cannot be avoided.

“In our experience, increases in land value are not solely attributable to a rezoning decision nor are decisions to rezone likely to be made without the landowner and/or developer’s significant investment in the process,” he said.

“The government’s decision to ignore the costs incurred in the pre-zoning phase will result in an effective tax rate that is higher than the 50 per cent prescribed in the legislation and could ultimately discourage private investment in the rezoning process.”

Subdividing can be profitable with research

Perth house prices continue to rise and Summit’s Senior Development Consultant, Adrian Johnson, says there’s no better time than now to look into subdivision strategy in that city.

“After three years of record growth, Perth remains the most affordable capital city in Australia to buy property in and on top of that, the state continues to face a housing and rental crisis, with Perth’s vacancy rate dipping to a historically low 0.4 percent.”

aussieproperty.com’s Mr Janes concludes it’s important to carefully consider the potential benefits and challenges before embarking on a subdivision project.

“Work with experienced professionals who can guide you through the process.

“With the right approach, subdivision can be a powerful tool for outperforming market growth and without the need of hoping for a significant market correction that may or may not arrive.”

Article Q&A

Is subdividing a profitable form of property investment?

Property experts say subdivision isn’t without its challenges and the process can be complex, expensive, and time consuming, however, the accelerated uplift in capital value will over the medium term increasingly eliminate risk. Adding value via subdivision is, over the long term, a powerful and relatively safe option worth considering.

Where are the best and worst places to subdivide in Perth?

Areas that have undergone rezoning or where there are proposed upgrading plans, such as shopping centre redevelopment sites, include Booragoon, Kardinya, Kensington, Wilson, Padbury, Craigie and Karrinyup. Areas such as Cannington, Beckenham, Gosnells, Kelmscott, Maddington and Armadale tend to have higher development costs in relation to site soil conditions and drainage requirements and, therefore, are not always favourable for developers.

Which are Melbourne’s best suburbs to subdivide property?

A Victorian Government report’s key findings on strategic locations for infill redevelopments identified Melbourne’s middle suburbs within a seven to 25 kilometre radius of the CBD, developed between 1950-1970s, and with close proximity to public transport and being outside areas with heritage overlays as being ideally located for subdivision. The study focused on Essendon, Preston, Burwood East, West Footscray and Doncaster.

Underquoting remains a major issue in the real estate industry, prompting the Victorian Government to launch a dedicated taskforce, while other states have issued relatively few, if any, infringements for the widespread practice.

The scourge of illegal underquoting continues to waste the time and money of property buyers and the varying levels of action – or inaction – by the states suggests the problem will not be eradicated soon.

An agent is underquoting the selling price of a residential property if they make a statement or publish an advertisement about its price that is less than their reasonable estimate of the property’s likely selling price.

Underquoting laws are designed to ensure that buyers don’t waste money and time on property inspections, getting reports and attending auctions for properties that will likely be out of their price range.

Media reports have suggested that up to 80 per cent of properties were estimated to be underquoted in Victoria and industry professionals have told API Magazine that the situation is no better in New South Wales or Queensland.

Despite these claims, the number of infringements being issued against perpetrators is relatively low in all states, while there were none issued in Queensland this year.

Allen Habbouchi, Head of Project Sales and Distribution, aussieproperty.com, said underquoting gives buyers false hope.

“Underquoting may actually deter buyers from entering the market at all, as they start to lose confidence and hope with the whole experience,” he said.

Mr Habbouchi said properties in Sydney were routinely underquoted and estimated it would rival the 80 per cent of properties advertised, as claimed with Victoria.

Deterrent value

Consumer Affairs Victoria (CAV) recorded 1,466 underquoting inquiries and complaints in the state from 1 July 2021 to 31 July 2022, with just 48 infringements and 171 official warnings eventuating. This compared to 977 contacts in 2019-20, and 1,218 in 2018-19.

NSW Fair Trading issued 161 penalty infringement notices for underquoting and related offences. Each case was fined $2,200. Agents in Sydney usually charge a commission of about 2 per cent on sales, meaning the revenue on a median house price in the city of $1.6m would be about $32,000.

Mr Habbouchi said the fines and current laws were not serving as a deterrent.

“Agents purposely underquote in order to get the numbers for auction but RP Data and CoreLogic also have a lot to answer for, as their valuation price guide varies between 20-30 per cent in some instances, which does not help consumers at all.”

Queensland’s Office of Fair Trading (OFT) said it monitors the marketplace and conducts targeted proactive compliance checks throughout the year.

“No trends or concerns in relation to underquoting have been identified and there have been no infringement notices issued for underquoting in Queensland this year.

“The OFT has received nine complaints this year from consumers raising matters associated with property pricing, including concerns about properties being marketed without a price, and where the initially listed sale price was later increased, however, the OFT is not aware of any consumers being financially impacted in relation to these.”

Melinda Jennison, Buyers Agent, Streamline Property Buyers, said in Brisbane, unlike Sydney and Melbourne, quote ranges are not provided to buyers prior to auction so there is rarely a price guide provided leading up to an auction.

“For private treaty sales, a lot of properties in Brisbane are still being listed without a price,” she said.

“Where buyers can be misled is when a property has been filtered at the back end of real estate portals with a price range that is well below the anticipated sale price.

“The result is that when buyers are searching up to a maximum prescribed value, properties that are well above that range are still appearing in the search feed for buyers and this is extremely misleading, but agents do it to attract more buyer interest.”

Timely taskforce

In Victoria, CAV has this week launched a $3.8 million taskforce to target unfair practices in the property market, including underquoting.