There is a chronic housing shortage in Western Australia but UDIA WA is offering up a clear set of actions to deliver more homes, faster.

Governments across the country continue to grapple with solutions to the housing supply crisis that is gripping the nation.

The need to address supply constraints has been ongoing, however, with recent figures from the Australian Bureau of Statistics confirming that Western Australia is the fastest growing state in Australia, and with housing affordability pressures continuing to mount, the need to take action is becoming even more critical.

According to CoreLogic, the median price of a new home in Perth has tipped over $650,000 and the rental vacancy rate is sitting at just 1.4 per cent.

In a bid to unlock much needed housing supply, UDIA WA recently released a report that identifies critical infrastructure requirements across three key growth corridors in Perth, which if funded could unlock land to bring forward supply and ultimately facilitate the delivery of close to 90,000 new homes.

These areas have been identified, because the primary constraint to getting residential land delivered in these areas is catalyst infrastructure such as wastewater pump stations and trunk mains, power substations and feeder networks, and intersection and road upgrades.

The new report builds on work that started with our pre-budget submission to the State Government late last year, which identified enabling infrastructure requirements in several areas.

Land not an unlimited resource

UDIA WA’s state election campaign has also identified how crucial it is that infrastructure coordination, funding and delivery align with development pipeline intentions for undeveloped urban zoned land and potential future urban land.

We are confident that proper coordination would enable early planning and greater certainty for residential projects and more efficient delivery of much needed homes.

The report takes our initial recommendations in the pre-budget submission and our election campaign platform and goes a step further in providing specific detail around what immediate priority enabling infrastructure is required and the initial investment needed within the next term of government, as well as longer term infrastructure requirements.

Excerpt from UDIA WA Growth Areas Infrastructure Requirements Report

The infrastructure requirements identified in this report are items/packages where industry believes there is a direct correlation between the infrastructure funding and accelerated delivery to market, and there is currently no funding committed (unless otherwise stated in the report).

A report like this is also important in highlighting that while there is land in Perth that has been zoned for urban or future urban use, it is not a simple process to bring that land to market and enable the delivery of housing.

Many people in the community have a misconception that urban zoned land is plentiful in a place like Perth, but the reality is, there are a myriad of constraints on this land from infrastructure to environmental issues that need to be addressed. In some cases, those constraints, particularly environmental, cannot be addressed and the land is fundamentally beyond access.

For the specific areas identified in the infrastructure requirements report, it is infrastructure limitations that are the key issue, but addressing these is possible.

To identify the critical infrastructure building blocks for key growth areas, a Working Group was formed with members of UDIA WA’s Infrastructure and Masterplanned Communities committees. It comprised developers, engineers and planners to ensure broad expertise and a holistic view.

The Working Group analysed different development areas across the Perth Metropolitan region which could deliver significant housing supply but that were constrained by a lack of infrastructure.

The intent is for the report to be regularly refreshed for infrastructure requirements in other growth areas, including Yanchep, Wungong, Karnup and the South West region to be considered further.

Infill development challenges

While unlocking new land for housing is one part of the puzzle, delivering housing across a range of areas in Perth is important.

However, the challenges in relation to infill development are different in nature, and our Infill Development and Precincts Committee continues to also identify opportunities to increase the viability of medium and high density infill projects and accelerate the delivery of supply in that sector as well.

Article Q&A

Where in Perth is major infrastructure development required?

UDIAWA’s Growth Areas Infrastructure Requirements Report has identified that an investment of $421 million in strategic infrastructure would unlock land to catalyse the delivery of new homes in North Ellenbrook and Bullsbrook, East Wanneroo, and East Wellard and Mundijong.

What is Perth’s vacancy rate and median property price?

According to CoreLogic, the median price of a new home in Perth has tipped over $650,000 and the rental vacancy rate is sitting at just 1.4 per cent.

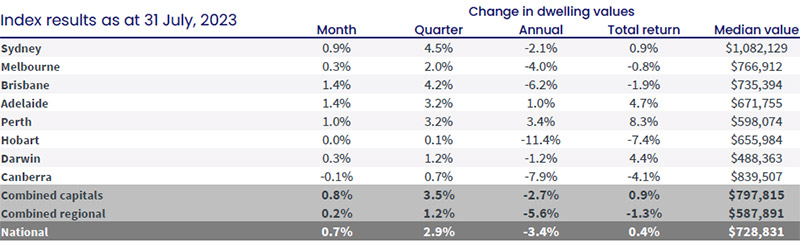

Property prices nationally rose 0.7 per cent in July, marking a fifth consecutive month of housing value recovery.

Adelaide and Perth were the standout property markets over the past month as real estate values nationally recorded a fifth consecutive month of increases.

CoreLogic’s national Home Value Index rose 0.7 per cent in July, as property prices continued to retrace the 9.1 per cent decline from the record highs of April 2022.

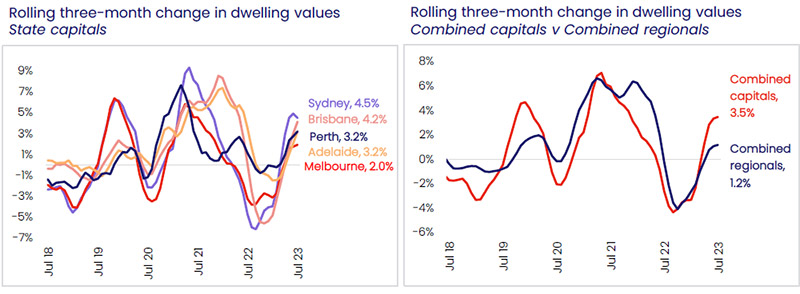

Nationally, prices are up 4.1 per cent since February but remain 5.3 per cent below the April 2022 peak. Only Perth, Adelaide and regional South Australia recorded a new cyclical high in dwelling values through July.

Regional values continued to lag behind the capitals, with the combined regionals index rising 0.2 per cent in July compared with a 0.8 per cent increase across the combined capitals index.

Every rest-of-state region recorded a smaller change in dwelling values through July relative to the capital city, reflecting milder housing demand across regional Australia as demographic patterns normalise.

Source: Corelogic.

CoreLogic Research Director, Tim Lawless, noted the most substantial reduction in growth has occurred in Sydney.

“After leading the upswing, the monthly pace of growth in Sydney housing values has halved from a recent high of 1.8 per cent in May to 0.9 per cent in July.

“Sydney has also seen a significant rise in the number of fresh listings added to the market, 9.9 per cent higher than the same time last year and 18.0 per cent above the previous five-year average.

“An increased flow of new listings provides more choice and may be working to reduce some of the urgency felt among prospective buyers,” he said.

Brisbane and Adelaide saw the monthly pace of growth accelerate in July, leading the pace of gains across the capitals with housing values up 1.4 per cent across both cities.

Source: Corelogic.

Although the trend in new listings has risen in these cities, Mr Lawless said the number remains well below levels from a year ago and the previous five-year average.

Canberra was the only capital city to record a decline in values in July, down 0.1 per cent, while Hobart values were unchanged.

Market conditions, however, continue to be solid in the face of the low supply of sales listings around the nation.

Property Investment Professionals of Australia (PIPA) Chair, Nicola McDougall, said the significant price falls simply did not materialise in many property markets – even with the most rapid increase in interest rates in a generation.

“Of course, part of the reason why prices have been strengthening is the significant number of overseas migrants – some half a million – who have landed on our shores within the past year or two, which is also causing rental markets to continue to struggle with a critical undersupply of stock,” she said.

Source: Corelogic.

Ms McDougall said as well as healthy market conditions, it appeared that the rising interest rate cycle may have come to an end.

“The Reserve Bank of Australia took its foot off the throttle in early July and held the cash rate steady at 4.1 per cent, which provided some confidence to property buyers around the nation,” Ms McDougall said.

“The June quarter inflation reading also came in well under market expectations at six per cent and with it highly possible we are at, or near, the peak of the cash rate.”

Sydney property price growing slowing

Sydney was the only city where the flow of fresh stock to market was higher than a year ago (+9.9%).

“Despite rapid rate rises and the so-called mortgage cliff, the market has carved itself into three distinct categories – the affordable, below $1.5 million corridors; the above $1.5 million areas; and the regionals.

“The everchanging landscape and dynamics is influenced by various factors such as economic conditions like the end of fixed rates and the high level of inflation, government policies, buyer preferences and affordability.

“Compound that with a strong immigration factor, and we have a stabilisation of value despite the negative economic and affordability outlook.

“Selling agents that were expecting a whole raft of properties to hit the market, as they report fielding increasing calls for market appraisals, are still to bring these properties on the market.

“Owners struggle to rationalise selling their properties, as they cannot qualify for a new loan at the same or higher level under the current lending constraints, and renting is also a struggle, with a strong shortage in most areas,” he said.

Brisbane housing in limited supply

Meighan Wells, Founder, Property Pursuit Advisors, said supply in Brisbane was as low as she had seen in 20 years.

She said people have been flocking to Queensland over the past two and a half years and no one is leaving.

“Pre-Covid, population fluctuations were common – people would come, and people would go.

“One of the common reasons for departure was to seek higher paying job opportunities interstate or overseas but with the ability to secure well-paying corporate jobs that have work-from-home, or hybrid arrangements, the requirement to relocate away from the Sunshine State has disappeared.

“The challenge for quality established housing supply is that no-one is selling until they can buy something else but no-one is leaving so we now have a bottleneck of owners who won’t sell until they can buy but can’t find anything to buy until someone leaves, and no-one is leaving and around and around it goes.”

Perth has strongest rental conditions

The strongest rental conditions nationally continue to be seen across the unit sector, where rents were up 2.9 per cent over the three months to July nationally, compared with a 1.9 per cent rise in house rents. Across the capital city and rest-of-state regions, the unit markets of Perth (4.3 per cent), Melbourne (4.0 per cent) and Brisbane (3.8 per cent) stand out with the fastest rate of rental growth over the rolling quarter.

That lack of supply was particularly keenly felt in the rental market, where investors had sold up in the face of tighter rental regulations and higher interest rates.

“Interest still remains very high for homes around the $500 to $600 range, with enquiries in the hundreds for each property, although that is still fewer than six months ago.

“City apartments are continuing to rent really quickly with a high amount of enquires and rents are still increasing, although not as dramatically as the last quarter.”

Mr White said a large majority of applicants are still desperately looking for a home.

“We see behaviour that reflects this constantly at home opens and in applications.”

Article Q&A

Have Australian property prices recovered?

CoreLogic’s national Home Value Index rose 0.7 per cent in July, as property prices continued to retrace the 9.1 per cent decline from the record highs of April 2022.

Which are the best performing Australian property markets?

Adelaide and Perth were the standout property markets over the past month as real estate values nationally recorded a fifth consecutive month of increases in to the end of July 2023.

Are rents rising in Australia?

The strongest rental conditions national continue to be seen across the unit sector, where rents were up 2.9 per cent over the three months to July nationally, compared with a 1.9 per cent rise in house rents. Across the capital city and rest-of-state regions, the unit markets of Perth (4.3 per cent), Melbourne (4.0 per cent) and Brisbane (3.8 per cent) stand out with the fastest rate of rental growth over the rolling quarter.

The Reserve Bank Governor Philip Lowe has used his final monthly meeting to leave interest rates on hold for a third successive month.

The RBA Board decided to leave the cash rate target unchanged at 4.10 per cent, pointing to subsiding inflation, broad economic uncertainty and earlier interest rate hikes still working their way through the economy.

The decision to hold came as little surprise, with all but one of 38 panellists from Finder’s RBA Cash Rate Survey believing the RBA would hold the cash rate steady in September.

Mr Lowe’s final Monetary Policy Decision said the Australian economy is experiencing a period of below-trend growth that is expected to continue for a while.

“High inflation is weighing on people’s real incomes and household consumption growth is weak, as is dwelling investment,” he said.

“Notwithstanding this, conditions in the labour market remain tight, although they have eased a little.

“Given that the economy and employment are forecast to grow below trend, the unemployment rate is expected to rise gradually to around 4.5 per cent late next year.

“Wages growth has picked up over the past year but is still consistent with the inflation target, provided that productivity growth picks up.”

He added that there is increased uncertainty around the outlook for the Chinese economy due to ongoing stresses in the property market there.

Unlike previous monthly rates announcements, Mr Lowe on Tuesday (5 September) issued a softer than usual notice that more rate hikes may be necessary to curb inflation.

“Some further tightening of monetary policy may be required to ensure that inflation returns to target in a reasonable timeframe, but that will continue to depend upon the data and the evolving assessment of risks,” he said, tempering his usual bullish sentiment with the ‘but’ on this occasion.

Little prospect of a rate cut

The rate hold is relatively good news for borrowers but the prospects of an imminent rate cut remain slim.

Economist Saul Eslake, of Corinna Economic Advisory, said the latest monthly CPI data for July show a further and welcome decline in headline inflation to 4.9 per cent, the lowest since February 2022, but still well above the RBA’s target range of 2 to 3 per cent.

“Underlying inflation also fell, but only to 5.6 per cent, even further above the target range, so there’s no need to tighten policy further but nor any reason to anticipate any reductions in interest rates any time soon,” he said.

Former Labor Government trade minister, Craig Emerson, of Emerson Economics, concurred, saying, “The RBA will consider it too early to ease and will maintain its pause position.”

David Robertson, Chief Economist, Bendigo Bank was less optimistic, saying a rate hike was more likely than a rate in coming months.

“The RBA appears comfortable holding the cash rate at 4.1 per cent ahead of the next quarterly CPI report out on 25 October 25.

“Another hike to 4.35 per cent remains the risk, as core services inflation remains stubbornly high, but not until November at the earliest.”

Many believe the cash rate will hold at 4.1 per cent now until the new year and will start to ease back, back to 3 percentage points range by the end of 2024 according to CBA’s Senior Economist Belinda Allen and Economist Stephen Wu. NAB economists believe there will likely be one more hike this year and Westpac’s Chief Economist Bill Evans believes we won’t see rate cuts till this time next year.

What does the RBA decision mean for property market?

The 29.2 per cent of borrowers deemed to be in mortgage stress remains notably lower than the levels witnessed during the financial turmoil of a decade or more ago when mortgage holders in stress reached a peak of 35.6 per cent in mid-2008.

But more concerning is the surge in the number of mortgage holders considered extremely at risk, which has now climbed to 1,017,000 (20.3 per cent). This figure significantly exceeds the long-term average of 15.4 per cent over the last 15 years and reflects an increase of more than 470,000 mortgage holders compared to a year ago, marking a 7.6 per cent rise.

Helen Avis, Director of Finance at Specialist Mortgage, said borrowers were refinancing in record numbers and increasingly turning towards mortgage brokers in an attempt to alleviate financial pressures.

Ms Avis said she expected the RBA to hold off on any further moves for several months as the current raft of increases gradually take effect.

“The majority of home price falls recorded last year have been reversed in 2023, with August marking the eight consecutive month of national home price growth. Strong demand and limited supply have offset the impact of rate rises that continued this year.

Eleanor Creagh, PropTrack Senior Economist, said subsiding momentum in inflation and consumer spending have eased pressure on the RBA to continue lifting interest rates as it tries to avoid a recession while taming inflation.

“The decision by the Reserve Bank to continue holding the cash rate steady in September is likely to maintain both buyer and seller confidence as the spring selling season begins, with home prices likely to continue lifting in the period ahead.

“The majority of home price falls recorded last year have been reversed in 2023, with August marking the eight consecutive month of national home price growth.

“Strong demand and limited supply have offset the impact of rate rises that continued this year.”

Rich Harvey, CEO, Propertybuyer, said as overstretched investors sell it could be a good time to enter the property market.

“Inflation is decreasing slowly as households are finally feeling the real pinch of significantly higher mortgage repayments, so there’s likely to be many discussions around the dinner table as to how households will adjust spending patterns to cope with higher rates.

“Discretionary spending is down and likely to stay low for next six months, and likely to see some investors offload investment properties if the drag on their budget is too strong.

“All this provides good buying opportunities for savvy buyers with financial means to secure more property,” Mr Harvey said.

A proposal put forward to impose a 45-day residency test in determining a person’s tax status, compared to the current 180 days, has sent shockwaves through Australian expatriate communities around the world.

Australian expatriates are in the sights of the Australian Treasury, with a proposal put forward to impose a 45-day residency test in determining a person’s tax status.

Under current law, residency is confirmed if a taxpayer spends more than 183 days in Australia, unless the Commissioner is satisfied they are genuinely living overseas.

Under the Board of Taxation’s proposed model, a long-term resident would cease to be a tax resident if they spent less than 45 days in Australia in the current income year, and less than 45 days in Australia in each of the two preceding income years. (The specific recommended guidelines to residency can be found at the end of this article, with full details available on the Treasury website).

Such a move would reverse the tax-free status of many expatriate Australians and have ramifications for their property holdings.

In justifying the change the Board said 45 days is longer than the normal annual leave period of four weeks, would ensure tourists and other short-term visitors did not become residents, and was comparable to jurisdictions such as New Zealand and the United Kingdom, which had 40 and 46 days respectively as their determinants of tax residency.

45-day ruling ‘would be investment deterrent’

Respondents to a survey conducted by Australasian Taxation Services (ATS) were far less enamoured with the proposals, with 93 per cent saying the ruling, if implemented, would affect their plans in regards to travel to Australia.

There were also implications for investment in Australia, with 52 per cent of the 861 respondents saying they would curtail their levels of investment in the country.

Steve Douglas, Executive Chairman, ATS, said the economic impact of unintended consequences could well be in the billions of dollars of lost economic activity in tourism and construction and further worsen the rental crisis by dampening activity from this important investor landlord group.

“A loss of property investment incentives is already wreaking havoc on the rental market in Australia and these further deterrents to housing supply mean landlords will continue to walk away from property investment and reduce rental supply.

“Landlords are being bashed from pillar to post, with stamp duty, land tax foreign buyer duties and surcharges and now this step aimed at greatly reducing the number of non-residents who will subsequently flee the property market.”

The reforms were intended, according to the Board, to “simplify the operation of the law significantly while mirroring the existing rules to a certain extent.”

Early indications from the public suggest the 80-page report on the new recommendations had not met that brief.

When asked about the clarity of the tax residency test of 45 days in Australia, an overwhelming 93 per cent of survey respondents said the new arrangements were “more confusing and difficult to interpret.”

Just over half (51 per cent) said the existing residency period of 180 days, or more, would be a sensible test of tax residency status.

The news rules also fail to provide an exception when it comes to time spent in the country. This also riled survey respondents, with a quarter saying work travel should be excluded and the same number again arguing that visitations to children of a former relationship who themselves can’t travel should also be exempt from the days-in-country count. More than a third (35 per cent) said funerals and compassionate family visits should be omitted from the tally.

ATS submitted their findings to Treasury before the 22 September consultation period closing date.

In their submission, they noted there have been two significant recent taxation law changes that have had a massive impact on expats’ and migrants’ capital gains in Australian property.

“It is not an unreasonable statement to suggest that these are having large scale unintended consequences as contributors to the current rental crisis in Australia, as anyone owning a property while living abroad is providing valuable rental stock for Australia’s booming population,” the ATS Modernising Individual Tax Residency Consultation Submission noted.

The submission singled out the 2012 removal of the 50 per cent capital gains tax discount for ownership periods while living overseas, and the 2021 removal of 100 per cent principal residence exemption if a property was sold while living overseas.

Australian residential property FIRB approvals

“At the same time, changes to the cost of FIRB (Foreign Investment Review Board) applications and the state governments’ introduction of foreign buyer and land tax surcharges, as well as increased difficulty for property finance options for foreign based buyers, have all combined to see a significant drop-off of foreign property investment activity,” the submission noted.

“The impact of these can be clearly seen through the drop off of FIRB applications since these changes started in 2015, and subsequent rapid escalation in 2016 and 2017.”

Proposed changes relating to assessment of an individual’s tax residency

1. Commencing Residency Test

Under the Commencing Residency Test, if you were present in Australia for 45 days or more in the current income year, then you will apply the ‘factor test’ looking at whether you would be a tax resident. This includes:

rights to reside permanently in Australia: Whether you have a permanent right to reside in Australia for immigration purposes

Australian accommodation: Whether there is a legal right or arrangement to access accommodation at any time during the income year (including rental properties, own home, living with parents or other relatives)

Australian family: Whether you have family in Australia

Australian economic interests: Whether you have an employment contract to work in Australia or carry out a business in Australia or have direct/indirect interests in Australian assets.

If you satisfy two or more factors from the above, you will be considered an Australian tax resident.

2. Ceasing Resident Test

If you were a tax resident in the previous income year, you will apply the Ceasing Residency Test.

As a start you will be considered a non-resident from the date of departure if you:

have been residing in Australia for the three prior income years

have been employed overseas with an employment period of over two years from commencement

have accommodation available in the place of employment for the entire employment period

spend less than 45 days in Australia for each income year of the employment period.

If the above does not apply –

If you are a short-term resident (resident for less than three* consecutive income years), you will be non-resident if you spend less than 45 days in Australia in the current income year and satisfy less than two factor tests (mentioned above).

If you are a long-term resident (resident for three* consecutive income years or more), you will be a non-resident if you spend less than 45 days in Australia this income year, and less than 45 days in Australia in each of the two previous income years.

Article Q&A

How many days do you need to live in Australia to be a tax resident?

Under current law, residency is confirmed if a taxpayer spends more than 183 days in Australia, unless the Commissioner is satisfied they are genuinely living overseas. Under the Treasury Board of Taxation’s proposed model, a long-term resident would cease to be a tax resident if they spent less than 45 days in Australia in the current income year, and less than 45 days in Australia in each of the two preceding income years.

Australians bemoan their own property taxation burdens but foreign buyers are hit with an array of imposing fees, taxes and surcharges that have somehow not scared them away from Australian real estate.

Interest in Australian property from international buyers continues to soar despite some eye-watering financial obstacles thrown up by the government.

PropTrack’s latest Overseas Search Report – October 2023 revealed that since its July report searches from abroad have continued to increase, with purchase searches up 11.5 per cent in the last three months and rent searches up 7.8 per cent.

Chinese buyers are particularly keen. According to the Foreign Investment Review Board’s latest report, Chinese buyers increased their spending on Australian homes by $1 billion in the past financial year, outlaying a whopping $3.4 billion on Aussie property.

The allure of Australia’s economic stability, rule of law, lifestyle and relative affordability is clearly enough for foreign buyers to overlook, or at least contend with, some staggering financial hurdles placed in their way.

Most Australians bemoaning their own stamp duty and land tax burdens would be surprised at the level of additional taxes and surcharges imposed upon foreign buyers and outraged if they had to cough up even a portion of those sums.

Speaking to API Magazine in Singapore, Ravin Chatlani, Director of Taxation, Australasian Taxation Services, said foreign buyers looking to acquire property in Australia had significant additional costs to factor in that the average Australian would be unaware of.

Fees and taxes for foreign property investors

The fee and charges imposed on foreign buyers could be tens or even hundreds of thousands of dollars more than that incurred by local buyers.

Mr Chatlani said overseas buyers were indeed still hugely interested in foreign property but said the costs involved were a deterrent to many.

The first cost they were up for was the Foreign Investment Review Board (FIRB) fee that amounted to $14,100 for every $1 million of the purchase price.

Then there’s the Foreign Buyers Duty (FBD) that comes on top of the regular stamp duty (and goes under different names in some states). That is levied at 8 per cent of the property price in New South Wales and Victoria and 7 per cent in Western Australia, South Australia and Queensland, and 3 per cent in Tasmania.

Ravin Chatlani, Director of Taxation, Australasian Taxation Services

For those foreign buyers still willing to cover those costs, there’s then the Absentee Land Tax Surcharge (ALTS) to place further strain on the budget.

“This varies from state to state but still costs the average international buyer tens of thousands of dollars,” Mr Chatlani said.

“While all land owners pay land tax, this is an additional one specific to overseas buyers.”

This tax is imposed on the land value, and in Queensland is 2 per cent with a tax-free threshold of $350,000, while in New South Wales (no exempt amount) and Victoria it is a more crippling 4 per cent.

This tax is not applied in Western Australia.

As of the start of 2024, Victoria will also be lowering the exemption threshold for all Australian and overseas landlords to just $50,000 from $300,000. The surcharge was 2 per cent for the 2020 to 2023 land tax years, 1.5 per cent for the 2017 to 2019 land tax years, and 0.5 per cent for the 2016 land tax year.

Mr Chatlani described said the added expenses were onerous and described the experience of a Singapore-based buyer.

“He was buying a $1.2 million apartment in Sydney and his land tax bill alone every year was $20,000, plus his strata fees and usual costs.

“The client said that even with the higher rental income, he felt he had nothing left at the end of it.”

But if regular stamp duty, plus the FIRB, FBD and ALTS weren’t spooky enough, there’s also the ghost tax, or vacancy tax as it is more formally known, to overcome.

For properties bought after 9 May 2017, a vacancy fee is applicable if the residential dwelling is not residentially occupied, genuinely available on the rental market, or rented out for six months or more in a 12-month period. The vacancy tax is usually the same as the FIRB application fee paid by investors when submitting a foreign investment application.

Why would any foreigner buy property in Australia?

So why is Australian property still so appealing to foreign buyers?

Mr Chatlani said every buyer had a different reason to purchase in Australia.

“Taking for example Singapore or Hong Kong buyers, with exception of perhaps parts of Sydney, buying in Australia is a smaller outlay.

“A townhouse in Melbourne or Brisbane, or even a house in Perth, for $1 million is a more attractive portfolio option than a small apartment in either of those cities.

“The richer investors from southeast Asia, from China, Taiwan, this is what they look at.

“For the investor in Shanghai where the average apartment price is A$1.5 million, they would gladly buy instead a $900,000 townhouse in Melbourne because it is cheap and they are expanding their property portfolio.”

The financial disincentives through Australian taxes and fees are also prevalent for foreigners in their own local markets.

“Here in Singapore for example, a local buying their second property is subjected to stamp duty of 20 per cent of the purchase price.”

Despite the various additional entry and holding costs, Mr Chatlani still felt the Australian property market was attractive to global investors due to the transparency of the market and stable rule of law that protects all parties within a property transaction.

“The way rental properties are managed in Australia is also very efficient and reliable and provides a complete service.

“Owning an Australian property can be a set and forget proposition.”

He added that education, potential retirement and migration, wealth preservation, relative affordability and potential currency advantages if the Aussie dollar was to rise against their own currency, were all key motivators for foreigners looking at property outside their home country.

Article Q&A

Are foreigners buying more Australian property?

According to the Foreign Investment Review Board’s latest report, Chinese buyers increased their spending on Australian homes by $1 billion in the past financial year, outlaying a whopping 3.4 billion on Aussie property. PropTrack’s latest Overseas Search Report – October 2023 revealed since its July report, searches from abroad have continued to increase, with purchase searches up 11.5 per cent in the last three months.

What extra fees and taxes do foreign property buyers have to pay in Australia?

Among an array of taxes and surcharges overseas buyers of Australian property have to pay, on top of regular stamp duty, are the FIRB, FBD and ALTS and a vacancy tax.

With housing affordability at its lowest level in three decades thanks to higher cost-of-living pressures, interest rate raises and healthy property prices, Perth’s property market is proving a standout.

Helen Avis, director of specialist mortgage at brokerage SMAT Services, said Perth was experiencing a massive boom generated by younger home buyers, with housing affordability better than it was in the late 2000s and early 2010s during the height of the mining investment boom.

Avis (pictured above left) said young home buyers had shown an increased interest in the property market during the pandemic.

“But post pandemic there has been a marked decline in first home buyers in Sydney and Melbourne, which we put down to affordability, rising interest rates and the difficulties of saving for a deposit.

“The opposite can be said about Brisbane and Perth, where there is still strong demand from the first home buyer market.”

Julie Kelley, sales and marketing manager at national real estate group aussieproperty.com, (pictured above centre) said across Australia there had been an increase in the number of first home buyers attending open homes with their parents, indicating the bank of mum and dad could be the key to entering the market.

East coast investors buying lower-priced Perth property

However, Kelley said Perth property in the lower price range, particularly in the outlying suburbs, was being snapped up by east coast investors.

“Unfortunately, this is resulting in first home buyers facing more competition for homes priced under $600,000 and they are being forced to broaden their search to the outskirt suburbs or consider buying smaller apartments and cottage homes,” Kelley said.

“The biggest increases in enquiries are from investors and buyers looking to upgrade their homes.

“There has been an enormous increase of interstate interest in Perth real estate particularly from Sydney and Melbourne.

“We have also seen a record night numbers of interstate migration and given Perth’s vacancy rate of 0.9% it’s difficult to secure rental properties, so many cashed up eastern states’ migrants are looking to purchase. “

Avis said many interstate buyers were guided by buyers’ advocates with limited local area knowledge or by big data, which could lead to poor long-term investment decisions.

“Off-the-plan developments hasn’t been popular for the past 12 months mainly due to the risk factors associated with the current state of the building and construction industry,” Avis said.

“Inner city suburbs and the western suburbs are still the most desirable locations for owner occupiers and investors, the north west coastal suburbs are also very popular.

“They are well established suburbs, close to the river and ocean, have excellent amenities, recreational facilities and public transport to the CBD and universities.”

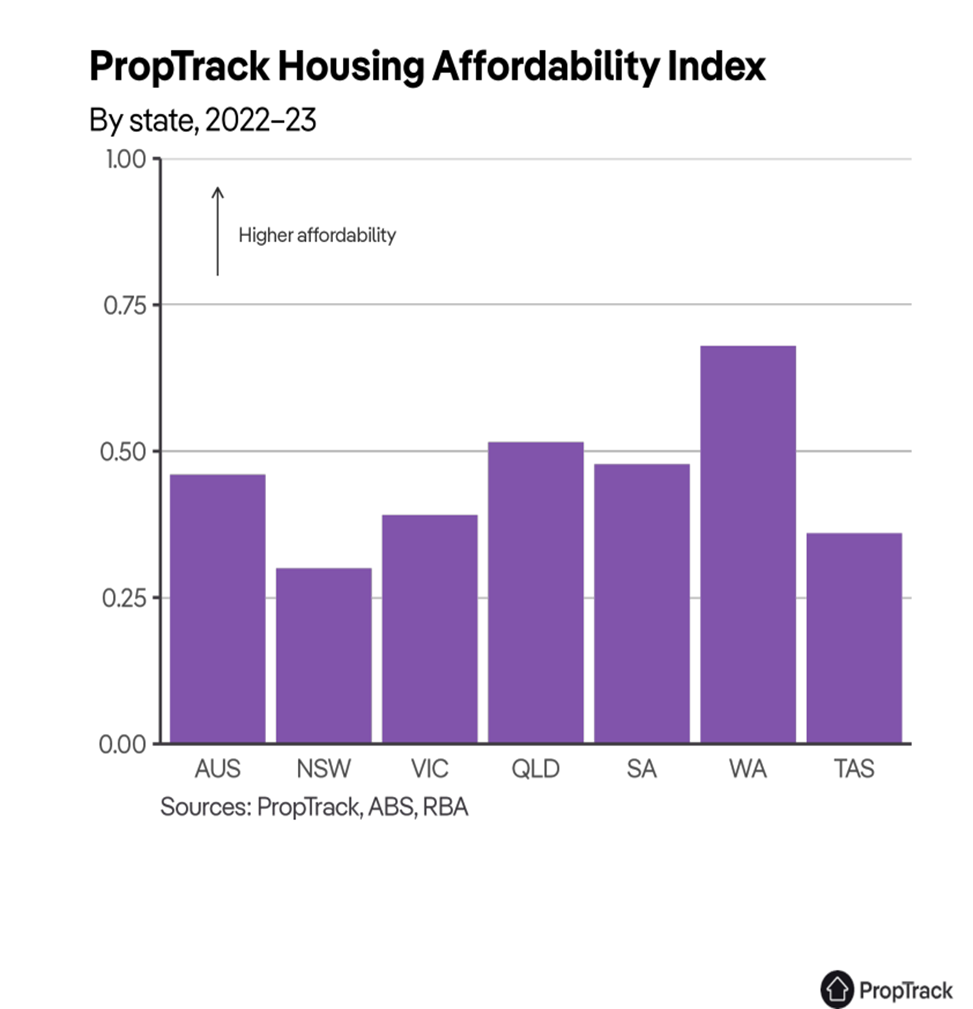

A recent PropTrack Housing Affordability Index 2023 report highlights just how dire affordability is now particularly in NSW, Tasmania, and Victoria, with Perth the most affordable state in Australia.

“That is a marked change from a decade ago, when Western Australia was the least affordable state from 2007-2010 amid the height of the mining investment boom,” the report states.

“[This is] the only time any state has displaced NSW as the least-affordable state.”

Peter Gavalas, a buyer’s agent from Resolve Property Solutions, (pictured above right) cautioned that fierce buyer competition amid the booming Perth property market could see some buyers settle for low-quality properties that they might one day regret owning.

“The bottom line is that, right now, the Perth property market doesn’t have enough supply to cater to all the demand,” Gavalas said.

“So buyers are reacting the same way they do in any boom – they’re compromising on quality, by settling for less desirable homes, such as ones with structural problems, or less desirable locations, such as on noisy main roads, because they fear they’ll never enter the market any other way.”

Gavalas said even though buyers were experiencing FOMO, it was likely they would suffer a case of buyer’s remorse in the years ahead if they compromised on quality.

“A better option would be to buy a higher-quality property with stronger resale value in a cheaper neighbouring suburb,” Gavalas said.

Capital gains tax is a minefield and knowing how to tip-toe through the maze unscathed is a crucial component of any successful property portfolio and investment strategy.

For many investors, the idea of handing over a sizeable chunk of a property sale profit to the Australian Taxation Office (ATO) is overwhelming, disheartening or even unjust.

However loathed it may be, CGT is a fundamental part of the property investment journey, so it pays to understand it and have a grasp of some ways to minimise its impact.

CGT is a tax on the capital gain made from the sale or disposal of assets, such as real estate, shares, and investment properties. The ATO considers most assets acquired after 20 September 1985 to be subject to CGT, although some exemptions apply.

Sydney-based Tax Manager for Australasian Taxation Services, Annie Zhu, said navigating the CGT landscape could be tricky and there were significant differences in how the tax was applied for resident and non-resident Australians.

“For tax residents, there’s a CGT discount applicable when the investment property is held for more than a year,” Ms Zhu said.

So far, so straight forward – until you move overseas.

“CGT discount is not available to foreign and temporary tax resident individuals for assets property held or acquired after 8 May 2012,” she explained.

“We need to use the market value on 8 May 2012 to calculate the CGT discount proportionally based on the number of days for those two separate periods when the property is held in Australia and while overseas.

“If there was no market value provided on 8 May 2012, during the periods of holding the property as a non-tax resident or temporary tax resident it is not eligible for any CGT discount.”

Calculating CGT

To calculate the capital gains tax liability, you need to determine the capital gain made from the disposal of an asset. The capital gain is generally the difference between the asset’s cost base (the purchase price, including associated costs) and the proceeds received from the sale.

The formula for calculating CGT is as follows:

Capital gain = sale proceeds – cost base

The tax is then applied to the capital gain at an individual’s marginal tax rate.

A CGT case study

Capital gains tax case for David, the returning expatriate

David purchased a residential property for $500,000 on 5 July 2001.

He moved to Hong Kong on 6 March 2003 and rented out the property, when the market value of the property was $650,000.

The market value of the property on 8 May 2012 was $850,000.

He returned back to Australia and became a tax resident on 24 May 2018 and the property continued to be rented out as an investment property.

On 21 June 2022 he signed the sale contract and sold the property for $1.25 million, and settlement occurred on 1 August 2022.

The CGT outcomes for David

Dates

Gross Capital Gain

Net Capital Gain

5/7/2001 – 6/3/2003

Property lived in (disregarded)

$0

$0

7/3/2003 – 6/3/2009

Main Residence CGT Exemption

(six years absentee provision)

$0

$0

7/3/2009 – 7/5/2012

CGT discounted

$69,180

$34,590

8/5/2012 – 23/5/2018

CGT non-discounted

$238,800

$238,800

24/5/2018 – 21/6/2022

CGT discounted

$161,200

$80,600

Total

$469,180

$353,990

CGT exemptions and concessions

As Ms Zhu highlighted, there are variations to the amount of tax applied based on a range of factors surrounding the property in question.

The first rule to know is that the primary place of residence (PPOR) is not subject to CGT.

Eligible small business owners may be entitled to various concessions, such as the 15-year exemption, 50 per cent active asset reduction, retirement exemption, and small business rollover.

These concessions aim to support entrepreneurship and encourage investment in small businesses.

For assets acquired before September 20, 1985, capital gains before this date are generally exempt. However, subsequent improvements made to the asset after this date may be subject to CGT.

Ms Zhu said the CGT six-year rule also offered a way out of paying CGT for some landlords while still earning rental income.

The rule allows owners to use their PPOR as an investment, by renting out for a period of up to six years. The caveat here is that it only applies if not deeming another property to be the main residence, as the ATO will only permit one CGT exempt main residence at a time.

If the property is sold within the six years, the owner would be exempt from paying CGT as they would if they sold the house they primarily lived in.

The benefit of the rule appeals to homeowners who want to make some extra money for the time that they are not, for whatever reasons, able to stay in their home – without prompting the need to pay CGT upon its eventual sale.

When a rental or investment property is sold at a loss position, those capital losses can only be used to offset/decrease any capital gains but not the ordinary income.

Determining the cost base

If the property was purchased as an investment property, the cost base is the original purchase price plus any other relevant expenses.

If the property was instead purchased as a main residence, and was subsequently rented out as an investment property, then the ATO resets the cost base of the property to be the market value of the property on the date when it became an investment property. Any initial purchases costs are accordingly disregarded.

If the property was sold as a non-resident, the main resident exemption is not applicable. This means the CGT is calculated from day one (the initial purchase price will be the cost base) regardless of whether the property was used as a main residence property previously or not. The six-year absentee provision does not apply either in this case.

Understanding the calculation methods, exemptions and concessions available is crucial for taxpayers to effectively manage their tax obligations.

By staying informed and seeking professional advice when necessary, taxpayers can navigate the complexities of CGT while ensuring compliance and optimising tax outcomes.

Article Q&A

What is capital gains tax?

Capital gains tax is a tax on the capital gain made from the sale or disposal of assets, such as real estate, shares, and investment properties.

Is there a cut-off date for capital gains tax?

The Australian Taxation Office (ATO) considers most assets acquired after September 20, 1985, to be subject to CGT, although some exemptions apply.

How is capital gains tax calculated?

To calculate the capital gains tax liability, you need to determine the capital gain made from the disposal of an asset. The capital gain is generally the difference between the asset’s cost base (the purchase price, including associated costs) and the proceeds received from the sale.

Can you rent a property out and avoid capital gains tax?

The CGT six-year rule also offered a way out of paying CGT for some landlords. The rule allows owners to use their PPOR as an investment, by renting out, for a period of up to six years. If the property is sold within the six years, the owner would be exempt from paying CGT as they would if they sold the house they primarily lived in.

Six Sydney property experts reveal the suburbs and property types real estate investors should be looking to buy in 2024.

The Sydney property market has undeniably become unaffordable to many, with a median dwelling value $300,000 above the next highest median, Canberra, and almost $400,000 above Melbourne’s.

But like all city property markets, it is a diverse real estate landscape with its mix of sour lemons and appetising fruit cocktails awaiting property investors.

Despite its wince-inducing median dwelling value of $1,139,375 the city as a whole last month still notched up another 0.3 per cent price uptick, according to CoreLogic.

With price trends still in the positive, some suburbs are still delivering the type of capital growth, complemented by high rental returns, that captures the attention of property investors.

Houses remain the preferred investment vehicle but unit prices have been outstripping houses in recent months.

PropTrack’s Senior Economist, Eleanor Creagh, on Friday (11 April) said that in Sydney, six of the top 10 suburbs where unit growth is outpacing house price growth this year are in the Inner West, Inner South West, or City and Inner South, namely Dulwich Hill, Mortdale, Rozelle, Bexley, Balmain and Petersham.

Of all the suburbs in Australia, the house price premium over units is the most extreme in Clontarf, Queens Park, Bellevue Hill, and Vaucluse, in Sydney’s Northern Beaches and Eastern Suburbs. In these suburbs, houses can cost almost 10 times as much as units, with the difference in value ranging from $3 to $8 million.

So where should property investors turn their attention in Sydney?

Six property experts spoke to API Magazine and shared their thoughts on the suburbs that offered the best prospects for medium-term return on investment.

From the top end of town to more affordable outskirt suburbs, here are the suburbs they think will have investors sipping cocktails on the beach in the future.

Sydney’s 2024 property investment hotspots

Aaron Downie, founder and buyers agent, Mackenzie Property Group

The East, Lower North Shore, and Northern Beaches could potentially see above-average capital growth

Suburbs like Coogee, Neutral Bay and Curl Curl really stand out. These areas, with median house values in the $3m to $4 million range, are known for their quality of life, access to amenities and strong demand from families, professionals and investors, which may drive property values up.

I anticipate units to continue outperforming in the Sydney market, driven by an upturn of investor interest, as well as by downsizers and those preferring the lifestyle Sydney offers over relocation alternatives.

Allen Habbouchi, Head of Project Sales & Distribution, aussieproperty.com

Sydney’s top three suburbs likely to keep delivering stronger than normal trends are Coogee, Kingsford and Kensington.

This is mainly due to their strategic positioning within 10km of the CBD, university campuses, beaches and infrastructure.

Two of our commentators named Coogee as a suburb worthy of property investor attention.

They offer lifestyle and investment opportunities to residents and investors alike.

Ultimately these factors could potentially contribute to deliver stronger than expected growth for houses and units.

Locations like Liverpool and Campbelltown are already seeing 17 per cent annual increases in searches and this renewed interest will flow on to higher prices with the increased demand.

Much of the outperformance of the luxury end of the market has been due to the immunity of that segment to interest rate rises compared to the lower quartile. With the rate cuts now priced into rate market into the end of the year and start of 2025, we expect some of the serviceability constraints and buffers to ease.

Five Dock is also a suburb seeing a lot higher search volumes, in Sydney’s Inner west, where the Sydney Metro West project station is underway, which will enhance its already good transport links. It is close to the CBD and is relatively affordability compared to other nearby locations.

The Agency, CEO of Real Estate, Matt Lahood

Sydney’s price trajectory is slowing due to high interest rates and people having less disposable income. People don’t have the borrowing power of previous years, which is reducing the rate of growth.

The most likely places to resist this price pressure are Alexandria, Burwood and, on the Central Coast, Kincumber.

Liam Carmody, General Manager, Palise Property

Despite the significant median price difference compared to other capital cities, outer suburbs in Sydney may not necessarily be the best performing.

This can be attributed to various factors, including infrastructure, amenities, employment opportunities and lifestyle preferences.

Inner suburbs often offer better access to amenities and employment hubs, attracting higher-income individuals willing to pay premium prices.

Additionally, limited supply and high demand in inner suburbs contribute to price growth. In contrast, outer suburbs may have more affordable housing but lack the same level of amenities and infrastructure, resulting in comparatively slower price growth.

Three suburbs positioned to deliver stronger than trend capital growth this year could include:

Surry Hills: An inner-city suburb experiencing gentrification and attracting young professionals and investors.

Marrickville: Known for its cultural diversity and vibrant lifestyle, with ongoing development projects driving demand.

Parramatta: Sydney’s second CBD undergoing significant infrastructure improvements and development, and offering investment opportunities.

Julian Khursigara, Partner, Search Party Property

We would expect demand for units to remain particularly strong in metro areas as affordability issues persist and investor interest picks up throughout the year.

Some recent industry surveys have indicated a growing trend of families opting to downsize in Sydney.

Along with seasoned Sydney investors returning to the market, this is probably another reason for the recent exuberance for units and townhouses.

By comparison, interstate investor attention is largely focused elsewhere, and first home buyers are also finding it increasingly difficult to break into the Sydney market.

Six property experts interviewed by API Magazine identified a range of suburbs where property prices were expected to deliver strong capital growth, ranging from affluent coastal areas like Coogee to outer suburban Endagine.

What is the median property price in Sydney?

Despite its wince-inducing median dwelling value of $1,139,375 the city as a whole last month still notched up another 0.3 per cent price uptick, according to CoreLogic.

With Perth property price growth widely tipped to exceed 10 per cent in 2024, Sydney and other interstate and international investors are finding the temptation irresistible and flocking to the city’s real estate.

Sydney, Melbourne and overseas buyers are setting their sights on Perth’s property market, which is widely anticipated to rise by another 10 per cent or more in 2024 after doing the same in 2023.

Properties are selling at a record pace in the West Australian capital, with a median selling time of a lightning quick eight days.

That’s twice as fast as this time last year and is being driven by a chronic shortage of properties on the market.

There were 5,011 listings on www.reiwa.com at the end of October, a 2.7 per cent increase on the 30-year low recorded in September, but 37.4 per cent lower than the same time last year.

Perth is also leading the charge nationally when it comes to property price growth.

While residential property values across Australia experienced a 0.9 per cent increase in October, Perth comfortably exceeded that (1.6 per cent), ahead of Brisbane (1.4 per cent) and Adelaide (1.3 per cent).

The Perth property market’s growth has been steady too, with dwellings rising in value by 4.6 per cent over the past quarter and 10.8 per cent over the past year, which is the strongest annual rise in the nation.

Delivering an Australian property market update in Hong Kong, Steve Douglas, Chairman of SMATS Group and Managing Director of Australasian Taxation Services and aussieproperty.com, said Western Australia’s population growth rate of 2.3 per cent since December last year was the highest in the nation and was driving property prices higher and quicker than anywhere else in the country.

“It’s different to past booms such as the early to mid-2000s in that it isn’t necessarily driven by the resources sector,” Mr Douglas said.

“The economy is strong but the city’s relative affordability is making it increasingly attractive for interstate investors and migrants looking for solid rent yields or, if they’re moving, an unmatched lifestyle that is making people choose WA over other states.”

Mr Douglas added that downsizing retirees were also behind a significant portion of the current growth cycle.

“The biggest thing happening in Australia at the moment is that there is a load of people downsizing in high-pried places like Sydney, in particular, and when they sell the home they have lived in there is no capital gains tax.

“That is creating a wave of Baby Boomer cash buyers undeterred by high interest rates moving to lifestyle-rich and more affordable cities such as Perth to enjoy their retirement.”

Buyers and agents alike are reporting a ‘feeding frenzy’ that is seeing properties advertised for $800,000 going for $100,000 or more extra.

Julie Kelley, Global Sales and Marketing Manager for aussieproperty.com, said the market is moving quickly with it intensifying markedly in just the last six weeks.

“I expect Perth property prices to exceed double-digit growth in 2024.

“We have already seen increases of 5 per cent or more in many Perth suburbs in less than two months, listings are massively down and dwelling approvals remain at decade-low levels, meaning stock availability is a real issue.”

The suburbs that saw the most growth in October were Mosman Park (up 3.8 per cent to $1,910,000), South Perth (up 2.7 per cent to $1,875,000), Manning (up 2.7 per cent to $945,000), Spearwood (up 2.7 per cent to $575,000) and Cooloongup (up 2.5 per cent to $458,500), according to REIWA.

The appeal of Perth to Sydney buyers has a strong financial logic behind it.

Portion of income required to meet home payments

The average Western Australian family contributes 35.0 per cent of their income towards mortgage repayments, compared to homeowners in New South Wales spending 56.0 per cent of their family earnings on mortgage payments.

FOMO taking grip as buyers compete

Backing up the sense of FOMO emerging in the Perth market, API Magazine spoke to a prospective buyer at a home open in Perth’s southern suburbs who spoke of the difficulty of picking up a property in the current market.

“I’ve been to more than a dozen home opens and put several offers in tens of thousands of dollars above the asking price and not gotten anything,” Keith Ashley of Hocking said.

“Agents have told me that in suburbs along the corridor to be linked by the new Thornlie to Cockburn rail line, such as Canning Vale and Jandakot, they have interstate buyers on standby ready to buy anything that becomes available before it goes to market.”

Ms Kelley said there had been an enormous increase of interstate interest in Perth real estate, particularly from Sydney and Melbourne.

“We have also seen a record level of interstate migration.

“Given Perth’s vacancy rate of 0.7 per cent and the difficulty in securing rental properties, so many cashed up eastern states migrants are looking to purchase, although off-the-plan developments haven’t been as popular over the past year due to the risk factors associated with the current state of the building and construction industry.”

“Ultimately, gross rental yields in excess of 5 per cent combined with a high likelihood of significant capital growth are proving too good to resist for interstate, as well as Asian and expatriate, buyers,” she said.

The vacancy rate in Perth has been below 1 per cent since August 2022, and shows no sign of changing in the short term.

Landlords nationally expanding their horizons

New research indicates the distance between where landlords live and where they invest almost doubled in the past year.

Mike Mortlock, Managing Director, MCG Quantity Surveyors, said his company’s latest analysis of their client data showed the average distance between where landlords live and where they invest has reached a staggering 1,502 kilometres to date in 2023. This year’s outcome is a near doubling of the same analysis in 2022, which showed an average of 857 kilometres between a landlord’s home and investment.

He said the rise of Western Australia on property investors’ collective radar was the main catalyst and cited regulatory measures in some other states as one of the propellants.

“Western Australia has become the centre of Australian property investment – there’s little doubt its popularity with real estate buyers from the east coast has increased the gap between home and investment.”

“WA is now considered among the nation’s most investor-friendly jurisdictions.

“Price is a factor too as some big capital city markets are now beyond the reach of everyday buyers but there remains a raft of ill-conceived legislative moves among east-coast political parties that is playing to Western Australia’s advantage.

“Talk among investors is that tenancy legislation, compliance costs and increased tax burdens in our most populous states are forcing their hand when deciding where to purchase or build an asset.”

Article Q&A

What will property prices do in 2024?

Many commentators are predicting Perth property prices to exceed double-digit growth in 2024, driven by downsizers, record migration, low supply and relative affordability.

What is the vacancy rate in Perth?

The vacancy rate in Perth is 0.7 per cent, has been below 1 per cent since August 2022, and shows no sign of changing in the short term.

Why are interstate investors buying property in Perth?

The average Western Australian family contributes 35.0 per cent of their income towards mortgage repayments, compared to homeowners in New South Wales spending 56.0 per cent of their family earnings on mortgage payments. Perth’s affordability and capital growth prospects are a major lure.

Foreign property buyer numbers have taken off, with international real estate investors shaking off their post-Covid blues and turning their attention to Australia.

Foreign buyers are returning to the Australian property in large numbers, with total transactions soaring by 27 per cent over the previous financial year.

The Australian Taxation Office on Friday (21 June) released its Register of foreign ownership of residential land, which showed that Victoria had become the preferred choice of foreign investors.

Foreign buyers spent $4.9 billion on 5,360 Australian dwellings in the financial year to 30 June 2023 (the most recent data available), with Victorian investment leaping a massive 32 per cent over a year.

Foreign buyers paid an average price of $914,000, which is just below the overall average price across the country of$959,300 in the March quarter, according to the Australian Bureau of Statistics.

The data also showed that buyers were expressing a degree of confidence in the Australian property market, with buyers far outstripping sellers.

They sold 1,119 homes, with a total value of $1.0 billion. It is noteworthy that the definition of sale also includes when a foreign buyer becomes a permanent resident or citizen, even if they don’t actually sell the property, so the actual sales number is inflated against the buyer figure.

The number of offshore buyers in New South Wales was flat, and actually decreased by 1 per cent, from 664 to 656. Meanwhile, the number of buyers in Queensland and Victoria jumped. The number of buyers in Queensland climbed 17 per cent, while the number of buyers in Victoria jumped 32 per cent, by about a third.

Source: ATO

While Queensland attracted more buyers over all, New South Wales attracted more millionaire buyers. Foreign buyers purchased 284 homes in New South Wales during the year that were worth at least $1 million, compared to only 200 in Queensland.

“Victoria got by far the most millionaire buyers, with 569 foreign buyer transactions worth over $1 million each.

Overseas buyers not super wealthy

A widely held perception that foreign buyers are wealthier than local buyers was dispelled by the data.

Residential properties with values under $1 million formed the majority of residential property purchase transactions, accounting for 78.2 per cent of property transactions in 2022-23. This is an increase compared to 75.4 per cent in 2021-22.

Nor did this investment lead to any significant population growth. Of the 5,360 purchase transactions in 2022–23, 164 registrants became a permanent resident or gained Australian citizenship during the year (and are included in these statistics).

Daniel Ho, Juwai IQI Co-Founder and Group Managing Director, said the 27 per cent increase in buying last year shows that overseas buyers were bouncing back after the travel slowdown during the pandemic.

Source: ATO

“Why do foreign buyers like Australia?

“This report, encompasses buyers from all over the world, including all parts of Asia, North America, South Africa, and the UK and Europe, and such a wide population has varying motivations, but they all have some things in common – they appreciate Australia’s strong economy, good education system, and attractive lifestyle.”

“In many cases, these buyers paid 7 per cent or 8 per cent of the purchase price on stamp duty and tens of thousands of dollars, or more, on foreign buyer application fees (compared to local buyers) and once they own their property, at least until they become permanent residents or citizens, they will pay an additional land tax every year.”

Mr Ho said Australia’s apparent popularity was actually reflective of a wider international trend.

“People have been moving to Australia in record numbers, and that shows up in the foreign buyer reports but it’s not just Australia, because we see the same thing happening in the US, Canada, Europe, and the UK.

“There is a significant wave of post-Covid migration as people act on plans they had to put on hold during the pandemic.

“We also see it in Southeast Asian countries like Thailand, which have seen rapid intake of their golden visa programs since the pandemic.

“If the Australian government succeeds in reducing the number of foreign students and other migrants coming to the country, we can expect foreign buying to be affected.”

There are signs that foreign buyers are expanding their search beyond the east coast of Australia.

Victoria, New South Wales and Queensland still represent 86.9 per cent of all sale transactions, making up 91.3 per cent of the value of sale transactions for the reporting period.

But this is down markedly from 2021–22, when Victoria, New South Wales and Queensland represented 97.0 per cent of all sale transactions and 97.8 per cent of the value.

Tracking purchases over five years shows that South Australia features among the top three states, along with Victoria and Queensland, when it comes to transactions on vacant land.

Foreign buyers still a small pool

Foreign buyers comprise just 1.1 per cent of residential property sales across Australia.

Terry Ryder, Managing Director, Hotspotting, told API Magazine, that the latest number actually underlined just how little foreign investment there is in Australian residential real estate.

“There may have been a 27 per cent annual rise in transactions, but that’s from a really low base.

“Foreign buyers have been slugged in major increases in taxes in recent years, a trend that continued with the latest Federal Budget and some of the state budgets.

“It’s resulted in fewer foreign investors compared to historical norms and that has impacted the supply of apartments.

“Foreign buyers were once a major source of off-the-plan sales that allowed high-rise developers to get sufficient pre-sales to secure finance and proceed with a major project.

“Using foreign buyers as a cash cow with no electoral consequences is very short-sighted and has contributed to the rental shortage and the overall undersupply of new dwellings.”